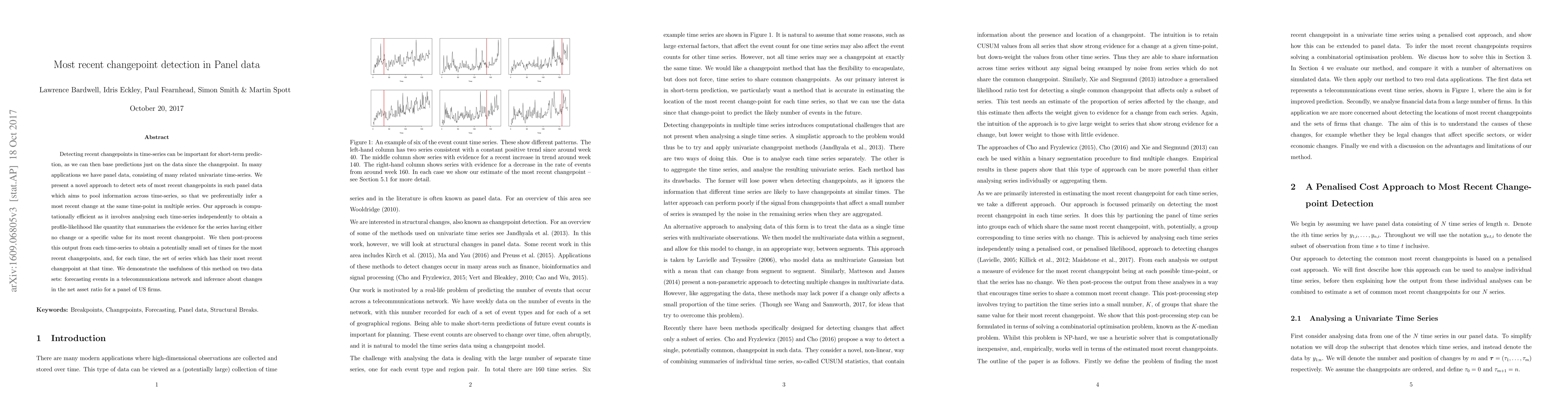

Most recent changepoint detection in Panel data

Publication

Metrics

AI Quick Summary

This paper presents a novel approach to detecting recent changepoints in panel data, focusing on pooling information across time-series to infer the most recent change at the same time-point.

Paper Preview

Abstract

Detecting recent changepoints in time-series can be important for short-term prediction, as we can then base predictions just on the data since the changepoint. In many applications we have panel data, consisting of many related univariate time-series. We present a novel approach to detect sets of most recent changepoints in such panel data which aims to pool information across time-series, so that we preferentially infer a most recent change at the same time-point in multiple series. Our approach is computationally efficient as it involves analysing each time-series independently to obtain a profile likelihood like quantity that summarises the evidence for the series having either no change or a specific value for its most recent changepoint. We then post-process this output from each time-series to obtain a potentially small set of times for the most recent changepoints, and, for each time, the set of series which has their most recent changepoint at that time. We demonstrate the usefulness of this method on two data sets: forecasting events in a telecommunications network and inference about changes in the net asset ratio for a panel of US firms.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0