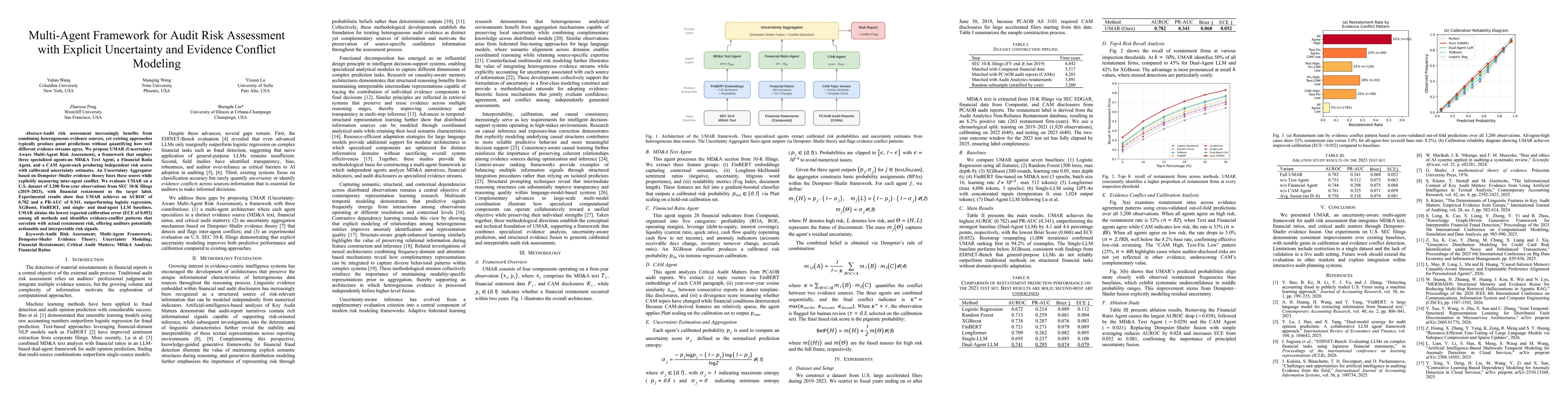

UMAR employs a four-component architecture: (1) MD&A Text Agent analyzes textual disclosures, (2) Financial Ratio Agent processes numerical financial indicators, (3) CAM Agent encodes Critical Audit Matters disclosures, and (4) an Uncertainty Aggregator based on Dempster–Shafer theory fuses independent risk scores while explicitly measuring inter-agent conflict. Each agent outputs calibrated uncertainty estimates; the aggregator combines these via evidential fusion to generate a final risk assessment with calibrated uncertainty and conflict signals. The evaluation uses a 3,200 firm-year SEC 10-K dataset (2019–2023) predicting restatement, comparing against baselines (logistic regression, XGBoost, FinBERT, and single/dual-agent LLM baselines). Calibration reliability is assessed with ECE, and evidence-conflict patterns are correlated with actual restatement risk to support interpretability for auditors.

Multi-Agent Framework for Audit Risk Assessment with Explicit Uncertainty and Evidence Conflict Modeling

Publication

Metrics

Quick Answers

What methodology did the authors use?

UMAR employs a four-component architecture: (1) MD&A Text Agent analyzes textual disclosures, (2) Financial Ratio Agent processes numerical financial indicators, (3) CAM Agent encodes Critical Audit Matters disclosures, and (4) an Uncertainty Aggregator based on Dempster–Shafer theory fuses independent risk scores while explicitly measuring inter-agent conflict. Each agent outputs calibrated uncertainty estimates; the aggregator combines these via evidential fusion to... More in Methodology →

What are the key results?

UMAR achieves AUROC 0.782 and PR-AUC 0.341 on the test set, outperforming baselines including logistic regression, XGBoost, FinBERT, and single/dual-agent LLM configurations. — UMAR attains the lowest expected calibration error (ECE = 0.052) among all evaluated methods, indicating well-calibrated risk probabilities. More in Key Results →

Why is this work significant?

The work demonstrates that explicit uncertainty modeling and inter-source conflict awareness via a multi-agent, evidence-theoretic fusion framework can improve predictive performance and calibration in audit risk assessment, while enhancing interpretability through detected evidence conflicts that align with real restatement risk. More in Significance →

What are the main limitations?

Evaluation is limited to a single dataset (SEC 10-K restatement task) and lacks live-audit setting validation. — The study does not test across multiple markets or regulatory regimes to assess generalizability. More in Limitations →

Paper Preview

Abstract

Audit risk assessment increasingly benefits from combining heterogeneous evidence sources, yet existing approaches typically produce point predictions without quantifying how well different evidence streams agree. We propose UMAR (Uncertainty-Aware Multi-Agent Risk Assessment), a framework that employs three specialized agents: an MD&A Text Agent, a Financial Ratio Agent, and a CAM Agent, each producing independent risk scores with calibrated uncertainty estimates. An Uncertainty Aggregator based on Dempster-Shafer evidence theory fuses these scores while explicitly measuring inter-agent conflict. We evaluate UMAR on a U.S. dataset of 3,200 firm-year observations from SEC 10-K filings (2019-2023), with financial restatement as the target label. Experimental results show that UMAR achieves an AUROC of 0.782 and a PR-AUC of 0.341, outperforming logistic regression, XGBoost, FinBERT, and single-agent and dual-agent LLM baselines. UMAR attains the lowest expected calibration error (ECE = 0.052) among all methods and identifies evidence-conflict patterns that correlate with actual restatement risk, offering auditors potentially actionable and interpretable risk signals.

Key Findings, in focus

Seven facets of this paper, analysed and brought into focus by AI.

The work demonstrates that explicit uncertainty modeling and inter-source conflict awareness via a multi-agent, evidence-theoretic fusion framework can improve predictive performance and calibration in audit risk assessment, while enhancing interpretability through detected evidence conflicts that align with real restatement risk.

- UMAR achieves AUROC 0.782 and PR-AUC 0.341 on the test set, outperforming baselines including logistic regression, XGBoost, FinBERT, and single/dual-agent LLM configurations.

- UMAR attains the lowest expected calibration error (ECE = 0.052) among all evaluated methods, indicating well-calibrated risk probabilities.

- Evidence-conflict patterns identified by the Dempster–Shafer fusion correlate with actual restatement risk, providing interpretable signals for auditors.

- Ablation study shows each agent contributes to performance; removing any single agent degrades AUROC and calibration.

The work demonstrates that explicit uncertainty modeling and inter-source conflict awareness via a multi-agent, evidence-theoretic fusion framework can improve predictive performance and calibration in audit risk assessment, while enhancing interpretability through detected evidence conflicts that align with real restatement risk.

Introduction of UMAR, a modular multi-agent framework that preserves source-specific representations (MD&A text, financial ratios, CAM disclosures) and fuses them with Dempster–Shafer evidence theory to quantify uncertainty and inter-agent conflict, enabling calibrated risk predictions and interpretable conflict-based signals.

First to integrate an explicit uncertainty-aware multi-agent architecture with Dempster–Shafer evidence fusion for audit risk assessment, including calibrated uncertainty outputs and interpretable conflict patterns across heterogeneous audit evidence streams.

- Evaluation is limited to a single dataset (SEC 10-K restatement task) and lacks live-audit setting validation.

- The study does not test across multiple markets or regulatory regimes to assess generalizability.

- Dependence on well-curated CAM disclosures may affect applicability in contexts with sparse narrative reporting.

- Extend evaluation to additional markets and time periods to test generalizability across regulatory environments.

- Integrate UMAR into interactive audit planning tools to assess real-time decision support and user trust.

- Explore alternative evidence theories and dynamic weighting schemes to further optimize fusion under varying data quality.

- Investigate robustness to adversarial or noisy evidence streams and assess scalability to larger, real-time datasets.

Discussion 0