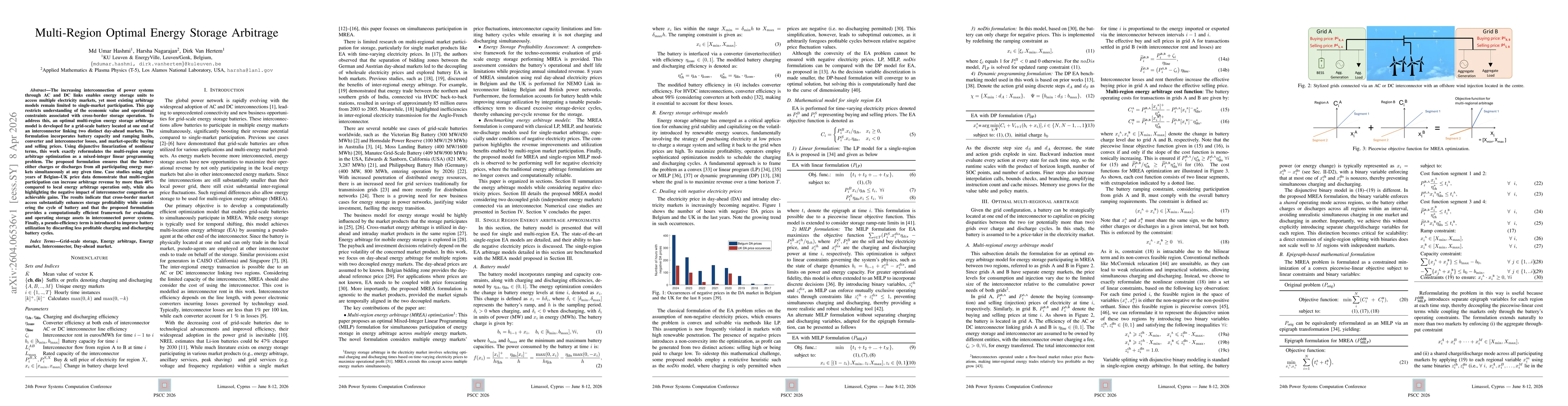

The increasing interconnection of power systems through AC and DC links enables energy storage units to access multiple electricity markets yet most existing arbitrage models remain limited to singlemarket participation This gap restricts understanding of the economic value and operational constraints associated with crossborder storage operation To address this an optimal multiregion energy storage arbitrage model is developed for a gridscale battery located at one end of an interconnector linking two distinct dayahead markets The formulation incorporates battery capacity and ramping limits converter and interconnector losses and marketspecific buying and selling prices Using disjunctive linearization of nonlinear terms this work exactly reformulates the multiregion energy arbitrage optimization as a mixedinteger linear programming problem The proposed formulation ensures that the battery either charges or discharges from all participating energy markets simultaneously at any given time Case studies using eight years of BelgianUK price data demonstrate that multiregion participation can increase arbitrage revenue by more than 40% compared to local energy arbitrage operation only while also highlighting the negative impact of interconnector congestion on achievable gains The results indicate that crossborder market access substantially enhances storage profitability while considering the cycle of battery and that the proposed formulation provides a computationally efficient framework for evaluating and operating storage assets in interconnected power systems Finally a pseudoefficiency term is introduced to improve battery utilization by discarding less profitable charging and discharging battery cycles

Discussion 0