Publication

Metrics

Paper Preview

Abstract

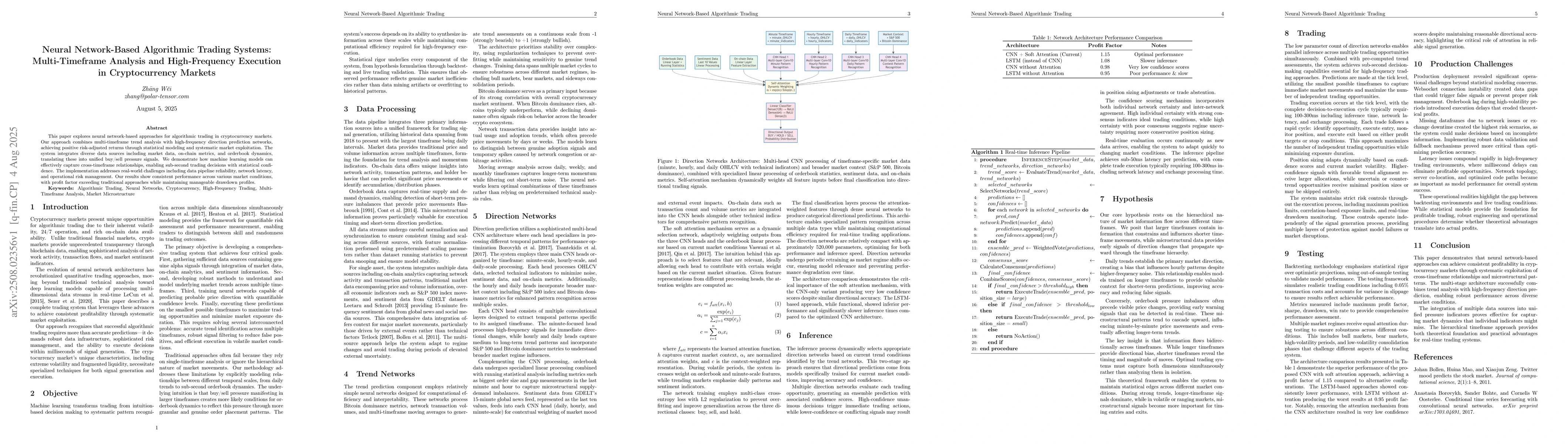

This paper explores neural network-based approaches for algorithmic trading in cryptocurrency markets. Our approach combines multi-timeframe trend analysis with high-frequency direction prediction networks, achieving positive risk-adjusted returns through statistical modeling and systematic market exploitation. The system integrates diverse data sources including market data, on-chain metrics, and orderbook dynamics, translating these into unified buy/sell pressure signals. We demonstrate how machine learning models can effectively capture cross-timeframe relationships, enabling sub-second trading decisions with statistical confidence.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0