Summary

We construct new multivariate copulas on the basis of a generalized infinite partition-of-unity approach. This approach allows - in contrast to finite partition-of-unity copulas - for tail-dependence as well as for asymmetry. A possibility of fitting such copulas to real data from quantitative risk management is also pointed out.

AI Key Findings

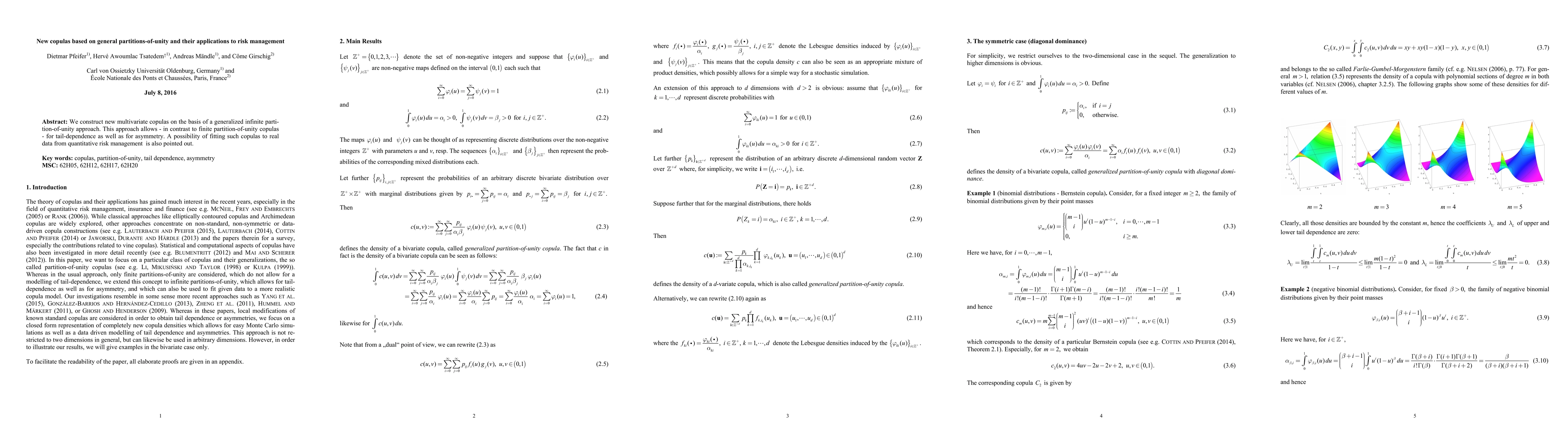

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Key Terms

unity

(0.394)

partition

(0.359)

pointed

(0.245)

tail

(0.228)

multivariate

(0.226)

asymmetry

(0.223)

real data

(0.219)

management

(0.215)

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Current Paper

Citations

References

Click to view

| Title | Authors | Year | Actions |

|---|

Comments (0)