01

MethodologyHow they did it

Simulation experiments with matrices having a structure similar to those described in [1,2] were conducted.

Research shows that noisy covariance matrices have little effect on portfolio optimization under linear constraints, but can lead to instability and degeneracy under non-linear constraints.

Research shows that noisy covariance matrices have little effect on portfolio optimization under linear constraints, but can lead to instability and degeneracy under non-linear constraints.

Simulation experiments with matrices having a structure similar to those described in [1,2] were conducted. More in Methodology →

Noise has relatively little effect on the solution of the classical portfolio problem (minimizing the portfolio variance under linear constraints). — The displacement of the solution due to noise is small, typically around 5-15% depending on the size of the portfolio and time series length. More in Key Results →

Empirical covariance matrices contain high amounts of noise, which can impact portfolio optimization and risk management practices. More in Significance →

The study only considered a specific type of noisy covariance matrix structure. — Further research is needed to explore the effects of different types of noise on portfolio optimization. More in Limitations →

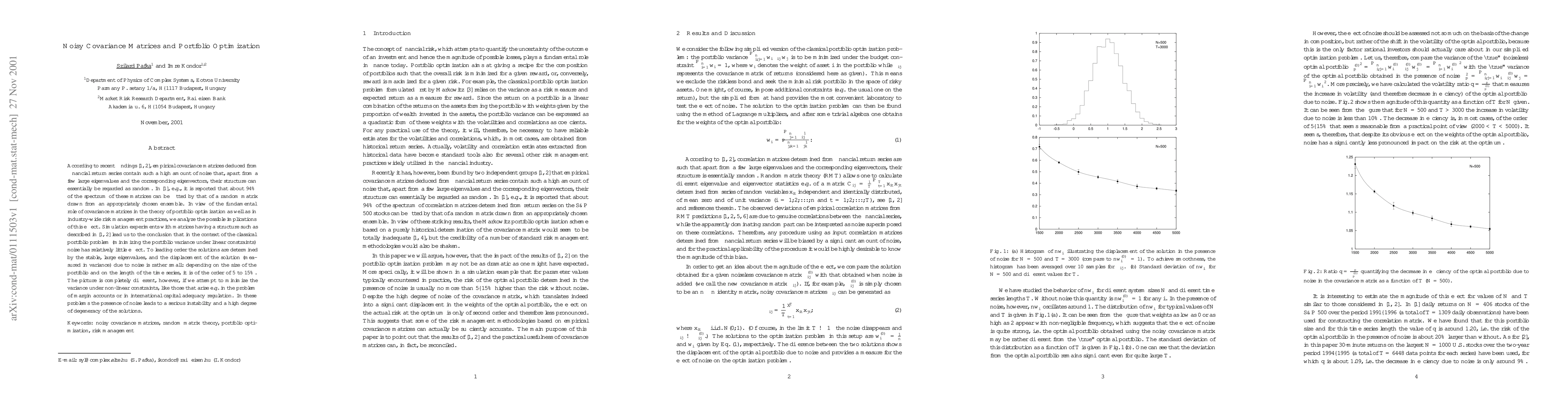

According to recent findings [1,2], empirical covariance matrices deduced from financial return series contain such a high amount of noise that, apart from a few large eigenvalues and the corresponding eigenvectors, their structure can essentially be regarded as random. In [1], e.g., it is reported that about 94% of the spectrum of these matrices can be fitted by that of a random matrix drawn from an appropriately chosen ensemble. In view of the fundamental role of covariance matrices in the theory of portfolio optimization as well as in industry-wide risk management practices, we analyze the possible implications of this effect. Simulation experiments with matrices having a structure such as described in [1,2] lead us to the conclusion that in the context of the classical portfolio problem (minimizing the portfolio variance under linear constraints) noise has relatively little effect. To leading order the solutions are determined by the stable, large eigenvalues, and the displacement of the solution (measured in variance) due to noise is rather small: depending on the size of the portfolio and on the length of the time series, it is of the order of 5 to 15%. The picture is completely different, however, if we attempt to minimize the variance under non-linear constraints, like those that arise e.g. in the problem of margin accounts or in international capital adequacy regulation. In these problems the presence of noise leads to a serious instability and a high degree of degeneracy of the solutions.

Seven facets of this paper, analysed and brought into focus by AI.

Empirical covariance matrices contain high amounts of noise, which can impact portfolio optimization and risk management practices.

Simulation experiments with matrices having a structure similar to those described in [1,2] were conducted.

Empirical covariance matrices contain high amounts of noise, which can impact portfolio optimization and risk management practices.

The study highlights the importance of considering the effects of noise on portfolio optimization, particularly under non-linear constraints.

This work is novel because it specifically addresses the impact of noisy covariance matrices on portfolio optimization and risk management practices.

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0