Nonlinear GARCH model and 1/f noise

Publication

Metrics

Paper Preview

Abstract

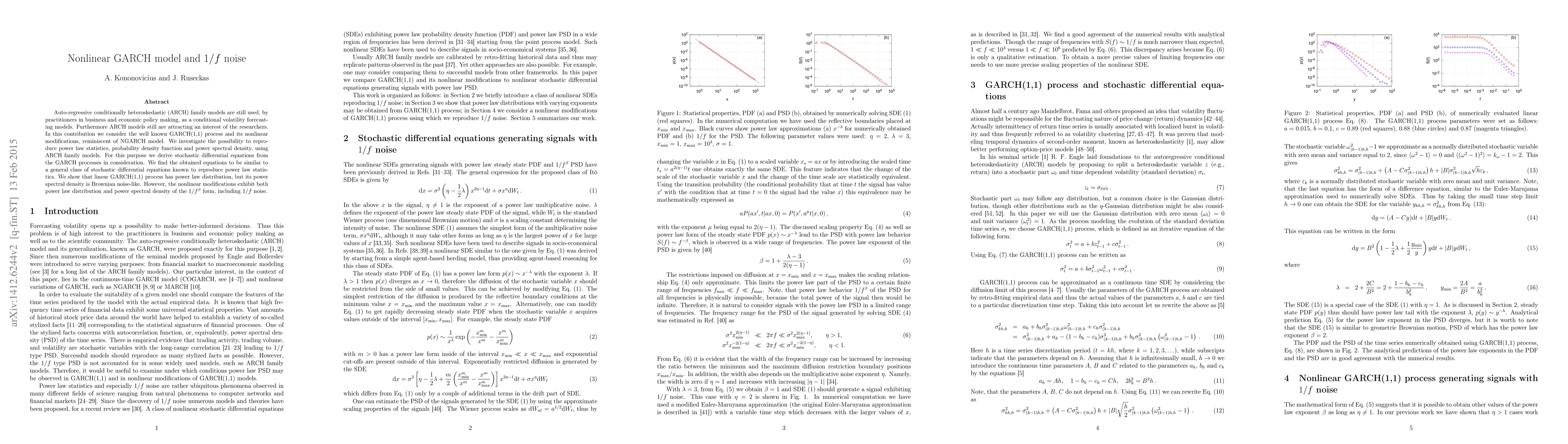

Auto-regressive conditionally heteroskedastic (ARCH) family models are still used, by practitioners in business and economic policy making, as a conditional volatility forecasting models. Furthermore ARCH models still are attracting an interest of the researchers. In this contribution we consider the well known GARCH(1,1) process and its nonlinear modifications, reminiscent of NGARCH model. We investigate the possibility to reproduce power law statistics, probability density function and power spectral density, using ARCH family models. For this purpose we derive stochastic differential equations from the GARCH processes in consideration. We find the obtained equations to be similar to a general class of stochastic differential equations known to reproduce power law statistics. We show that linear GARCH(1,1) process has power law distribution, but its power spectral density is Brownian noise-like. However, the nonlinear modifications exhibit both power law distribution and power spectral density of the power law form, including 1/f noise.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0