Nonparametric estimation of the jump-size distribution for a stochastic storage system with periodic observations

Publication

Metrics

AI Quick Summary

This paper introduces a non-parametric estimator for the jump-size distribution in a stochastic storage system with periodic observations, using characteristic function inversion. It analyzes the convergence rate and bias-variance tradeoff, demonstrating bounded risk in terms of mean squared error for a class of continuous distributions.

Paper Preview

Abstract

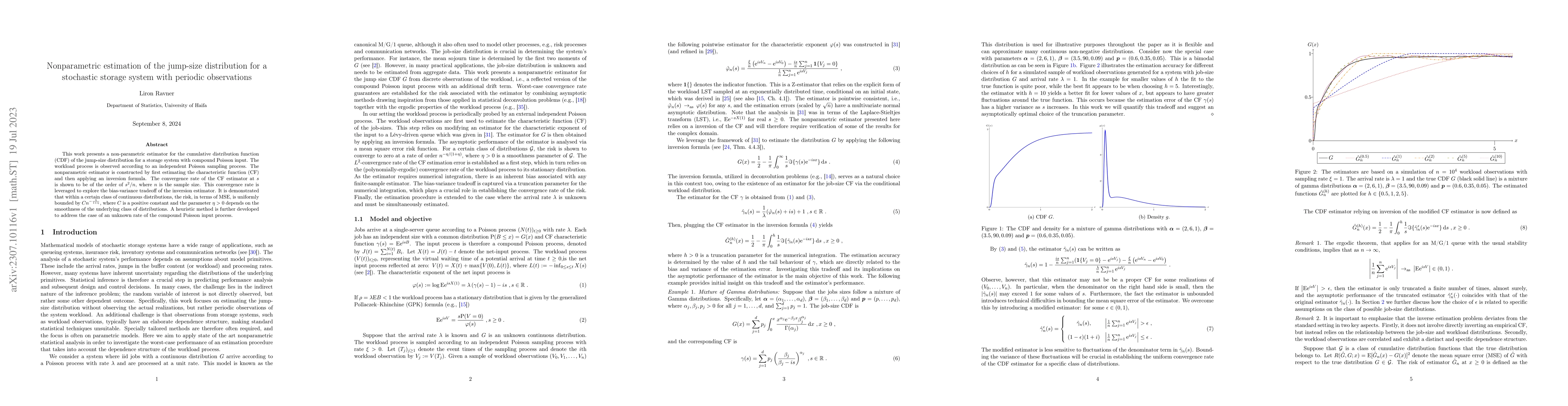

This work presents a non-parametric estimator for the cumulative distribution function (CDF) of the jump-size distribution for a storage system with compound Poisson input. The workload process is observed according to an independent Poisson sampling process. The nonparametric estimator is constructed by first estimating the characteristic function (CF) and then applying an inversion formula. The convergence rate of the CF estimator at $s$ is shown to be of the order of $s^2/n$, where $n$ is the sample size. This convergence rate is leveraged to explore the bias-variance tradeoff of the inversion estimator. It is demonstrated that within a certain class of continuous distributions, the risk, in terms of MSE, is uniformly bounded by $C n^{-\frac{\eta}{1+\eta}}$, where $C$ is a positive constant and the parameter $\eta>0$ depends on the smoothness of the underlying class of distributions. A heuristic method is further developed to address the case of an unknown rate of the compound Poisson input process.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0