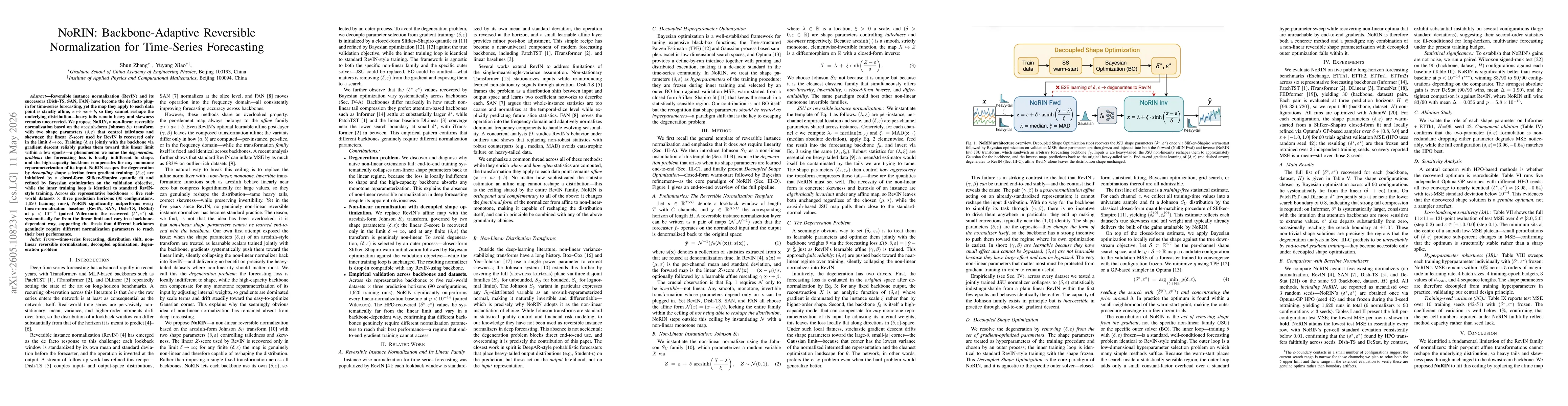

Reversible instance normalization (RevIN) and its successors (Dish-TS, SAN, FAN) have become the de facto plug-in for time-series forecasting, yet the map they apply to each data point is strictly affine, $x \mapsto ax+b$, so they cannot reshape the underlying distribution -- heavy tails remain heavy and skewness remains uncorrected. We propose NoRIN, a non-linear reversible normalization based on the arcsinh-form Johnson $S_U$ transform with two shape parameters $(δ,\varepsilon)$ that control tailedness and skewness; the linear $Z$-score used by RevIN is recovered only in the limit $δ\to \infty$. Training $(δ,\varepsilon)$ jointly with the backbone via gradient descent reliably pushes them toward this linear limit within a few epochs -- a phenomenon we name the degeneration problem: the forecasting loss is locally indifferent to shape, and the high-capacity backbone compensates for any monotone reparameterization of its input. NoRIN escapes the degeneration by decoupling shape selection from gradient training: $(δ,\varepsilon)$ are initialized by a closed-form Slifker-Shapiro quantile fit and refined by Bayesian optimization on the validation objective, while the inner training loop is identical to standard RevIN-style training. Across six representative backbones x five real-world datasets x three prediction horizons (90 configurations), decoupled shape optimization recovers $(δ^\star,\varepsilon^\star)$ that sit systematically far from the linear limit, with values that vary in a backbone-dependent way. This empirically supports the central thesis: different backbones genuinely require different normalization parameters to reach their best performance.

Discussion 0