Nowcasting Madagascar's real GDP using machine learning algorithms

Publication

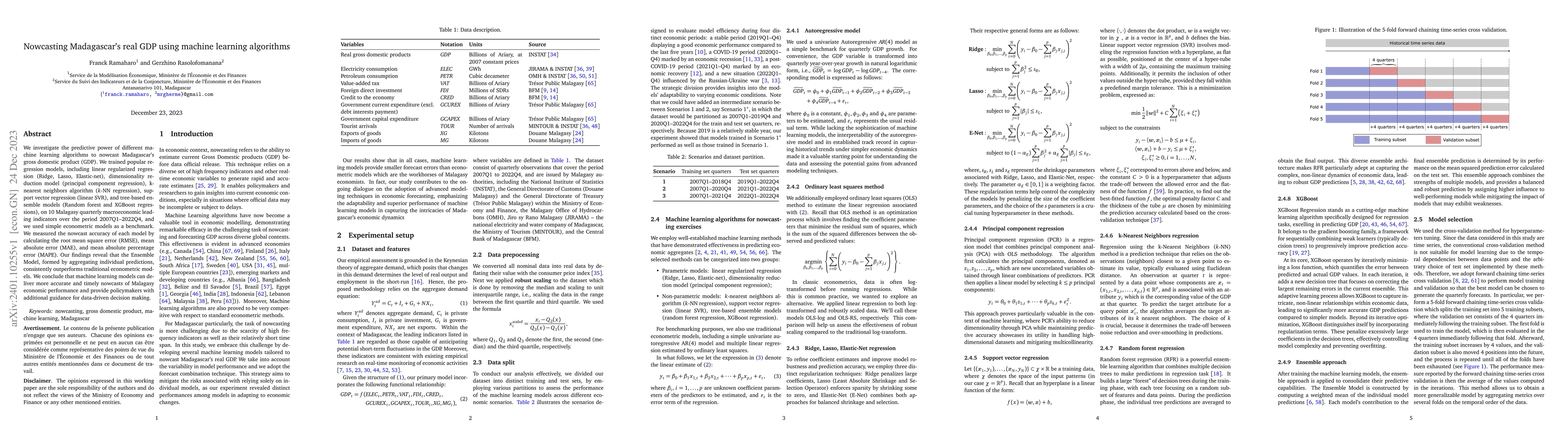

Metrics

AI Quick Summary

This study evaluates various machine learning algorithms for nowcasting Madagascar's GDP, finding that ensemble models like XGBoost outperform traditional econometric models, offering more accurate and timely economic forecasts to support policy decisions.

Paper Preview

Abstract

We investigate the predictive power of different machine learning algorithms to nowcast Madagascar's gross domestic product (GDP). We trained popular regression models, including linear regularized regression (Ridge, Lasso, Elastic-net), dimensionality reduction model (principal component regression), k-nearest neighbors algorithm (k-NN regression), support vector regression (linear SVR), and tree-based ensemble models (Random forest and XGBoost regressions), on 10 Malagasy quarterly macroeconomic leading indicators over the period 2007Q1--2022Q4, and we used simple econometric models as a benchmark. We measured the nowcast accuracy of each model by calculating the root mean square error (RMSE), mean absolute error (MAE), and mean absolute percentage error (MAPE). Our findings reveal that the Ensemble Model, formed by aggregating individual predictions, consistently outperforms traditional econometric models. We conclude that machine learning models can deliver more accurate and timely nowcasts of Malagasy economic performance and provide policymakers with additional guidance for data-driven decision making.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0