Publication

Metrics

AI Quick Summary

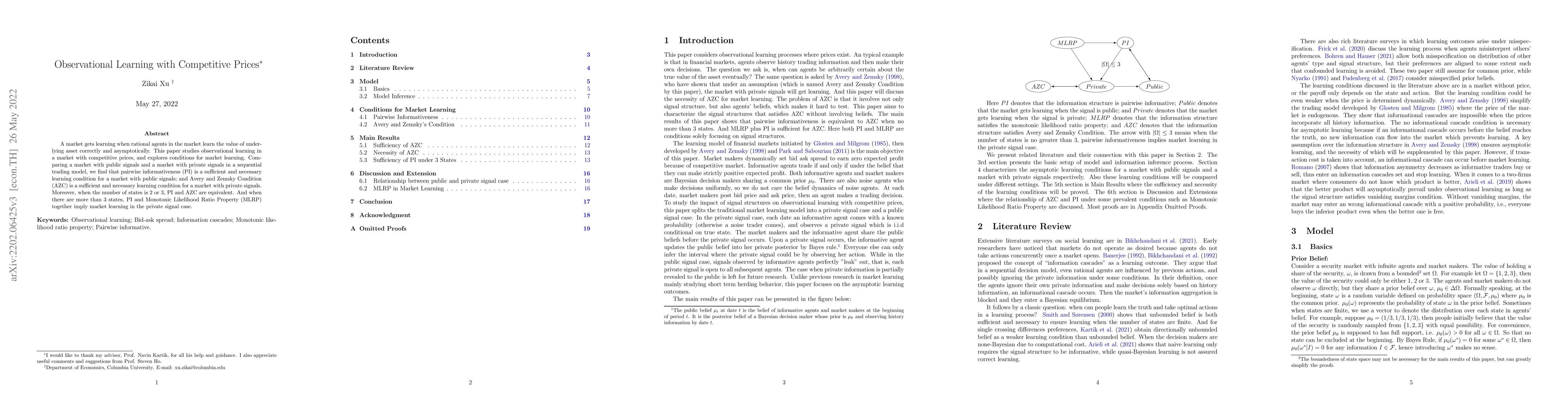

Researchers studied how people learn asset values through observable information in markets with public and private signals, finding that certain conditions imply learning; the findings have implications for understanding market behavior and price discovery.

Paper Preview

Abstract

Will people eventually learn the value of an asset through observable information? This paper studies observational learning in a market with competitive prices. Comparing a market with public signals and a market with private signals in a sequential trading model, we find that Pairwise Informativeness (PI) is the sufficient and necessary learning condition for a market with public signals; and Avery and Zemsky Condition (AZC) is the sufficient and necessary learning condition for a market with private signals. Moreover, when the number of states is 2 or 3, PI and AZC are equivalent. And when the number of states is greater than 3, PI and Monotonic Likelihood Ratio Property (MLRP) together imply asymptotic learning in the private signal case.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0