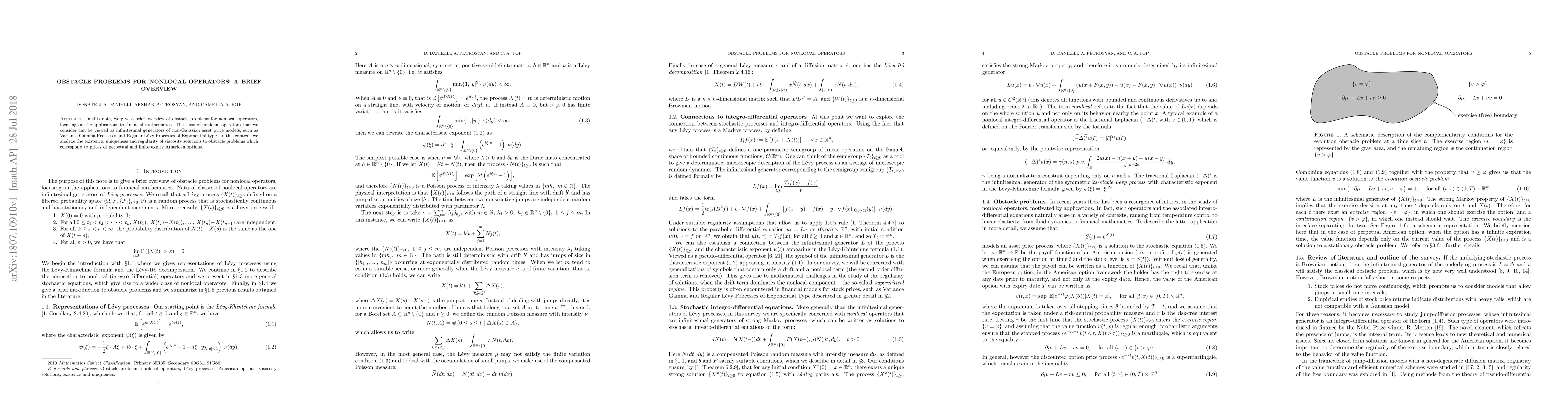

Obstacle problems for nonlocal operators: A brief overview

Publication

Metrics

AI Quick Summary

This paper provides a concise overview of obstacle problems associated with nonlocal operators, emphasizing their application in financial mathematics. It discusses the existence, uniqueness, and regularity of viscosity solutions for perpetual and finite expiry American options, linked to non-Gaussian asset price models like Variance Gamma Processes.

Paper Preview

Abstract

In this note, we give a brief overview of obstacle problems for nonlocal operators, focusing on the applications to financial mathematics. The class of nonlocal operators that we consider can be viewed as infinitesimal generators of non-Gaussian asset price models, such as Variance Gamma Processes and Regular L\'evy Processes of Exponential type. In this context, we analyze the existence, uniqueness and regularity of viscosity solutions to obstacle problems which correspond to prices of perpetual and finite expiry American options. Complete proofs can be found in arXiv:1709.10384, where these results have originally appeared.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0