Online learning algorithms continually update their models as data arrive,

making it essential to accurately estimate the expected loss at the current

time step. The prequential method is an effective estimation approach which can

be practically deployed in various ways. However, theoretical guarantees have

previously been established under strong conditions on the algorithm, and

practical algorithms have hyperparameters which require careful tuning. We

introduce OEUVRE, an estimator that evaluates each incoming sample on the

function learned at the current and previous time steps, recursively updating

the loss estimate in constant time and memory. We use algorithmic stability, a

property satisfied by many popular online learners, for optimal updates and

prove consistency, convergence rates, and concentration bounds for our

estimator. We design a method to adaptively tune OEUVRE's hyperparameters and

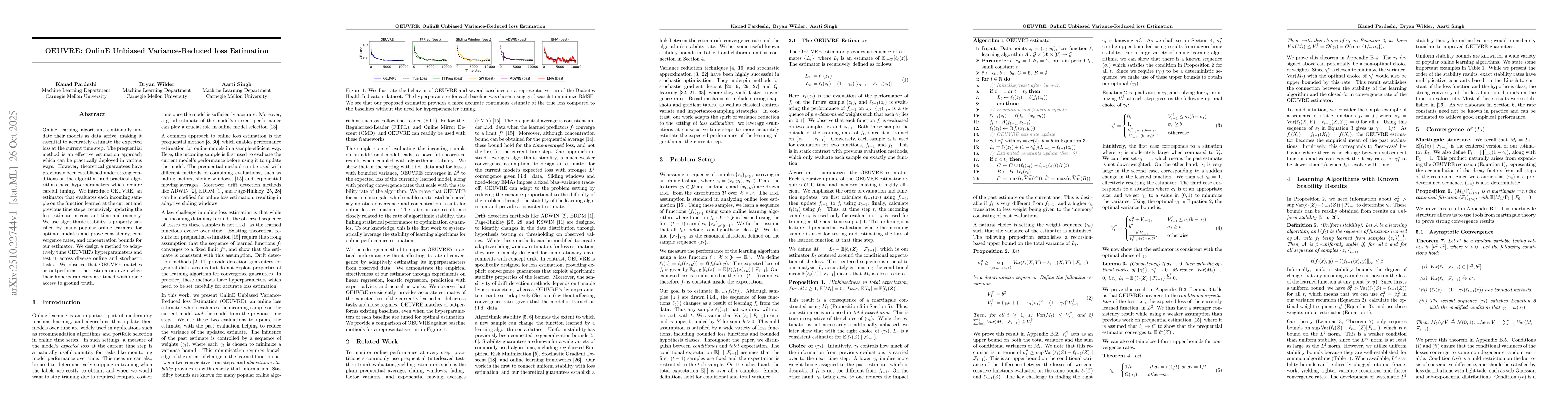

test it across diverse online and stochastic tasks. We observe that OEUVRE

matches or outperforms other estimators even when their hyperparameters are

tuned with oracle access to ground truth.

Discussion 0