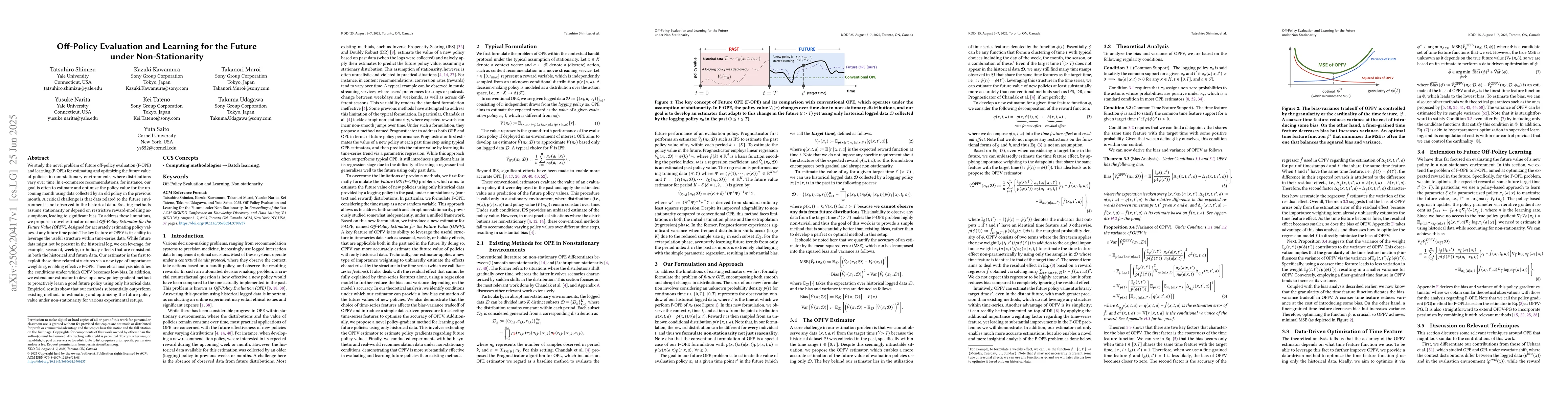

We study the novel problem of future off-policy evaluation (F-OPE) and

learning (F-OPL) for estimating and optimizing the future value of policies in

non-stationary environments, where distributions vary over time. In e-commerce

recommendations, for instance, our goal is often to estimate and optimize the

policy value for the upcoming month using data collected by an old policy in

the previous month. A critical challenge is that data related to the future

environment is not observed in the historical data. Existing methods assume

stationarity or depend on restrictive reward-modeling assumptions, leading to

significant bias. To address these limitations, we propose a novel estimator

named \textit{\textbf{O}ff-\textbf{P}olicy Estimator for the \textbf{F}uture

\textbf{V}alue (\textbf{\textit{OPFV}})}, designed for accurately estimating

policy values at any future time point. The key feature of OPFV is its ability

to leverage the useful structure within time-series data. While future data

might not be present in the historical log, we can leverage, for example,

seasonal, weekly, or holiday effects that are consistent in both the historical

and future data. Our estimator is the first to exploit these time-related

structures via a new type of importance weighting, enabling effective F-OPE.

Theoretical analysis identifies the conditions under which OPFV becomes

low-bias. In addition, we extend our estimator to develop a new policy-gradient

method to proactively learn a good future policy using only historical data.

Empirical results show that our methods substantially outperform existing

methods in estimating and optimizing the future policy value under

non-stationarity for various experimental setups.

Discussion 0