On Optimal Retirement (How to Retire Early)

Publication

Metrics

Paper Preview

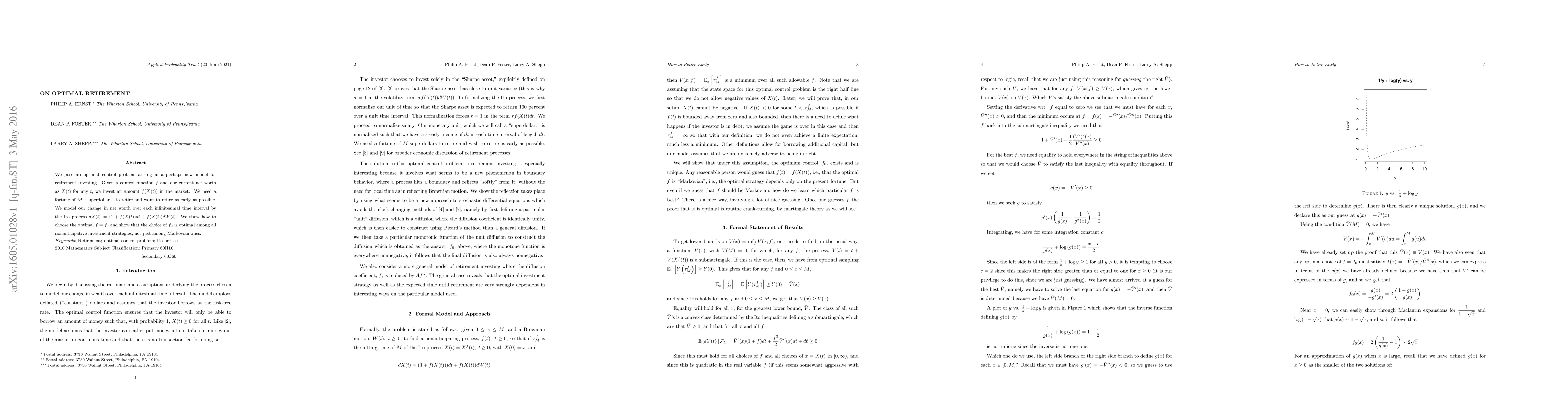

Abstract

We pose an optimal control problem arising in a perhaps new model for retirement investing. Given a control function $f$ and our current net worth as $X(t)$ for any $t$, we invest an amount $f(X(t))$ in the market. We need a fortune of $M$ "superdollars" to retire and want to retire as early as possible. We model our change in net worth over each infinitesimal time interval by the Ito process $dX(t)= (1+f(X(t))dt+ f(X(t))dW(t)$. We show how to choose the optimal $f=f_0$ and show that the choice of $f_0$ is optimal among all nonanticipative investment strategies, not just among Markovian ones.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0