On the distribution of the sum of dependent standard normally distributed random variables using copulas

Publication

Metrics

AI Quick Summary

This paper computes the distribution of the sum of two dependent standard normal random variables using copulas to model their dependency. It derives analytical expressions for the joint probability density function under various copulas and evaluates the cumulative distribution function numerically, showing significant differences among copulas, especially at higher quantiles.

Paper Preview

Abstract

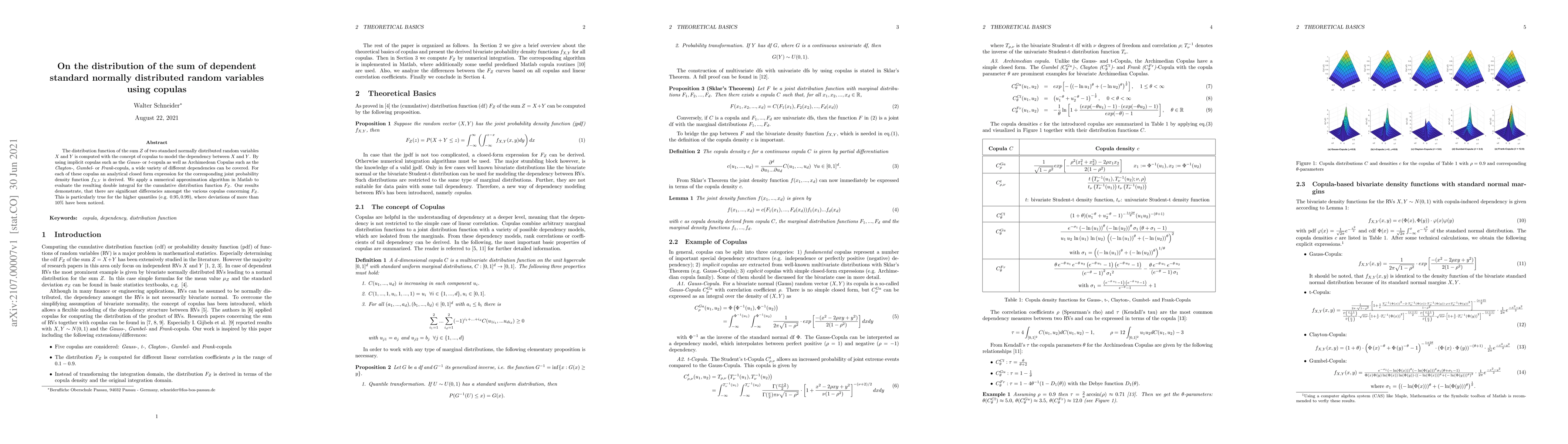

The distribution function of the sum $Z$ of two standard normally distributed random variables $X$ and $Y$ is computed with the concept of copulas to model the dependency between $X$ and $Y$. By using implicit copulas such as the Gauss- or t-copula as well as Archimedean Copulas such as the Clayton-, Gumbel- or Frank-copula, a wide variety of different dependencies can be covered. For each of these copulas an analytical closed form expression for the corresponding joint probability density function $f_{X,Y}$ is derived. We apply a numerical approximation algorithm in Matlab to evaluate the resulting double integral for the cumulative distribution function $F_Z$. Our results demonstrate, that there are significant differencies amongst the various copulas concerning $F_Z$. This is particularly true for the higher quantiles (e.g. $0.95, 0.99$), where deviations of more than $10\%$ have been noticed.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0