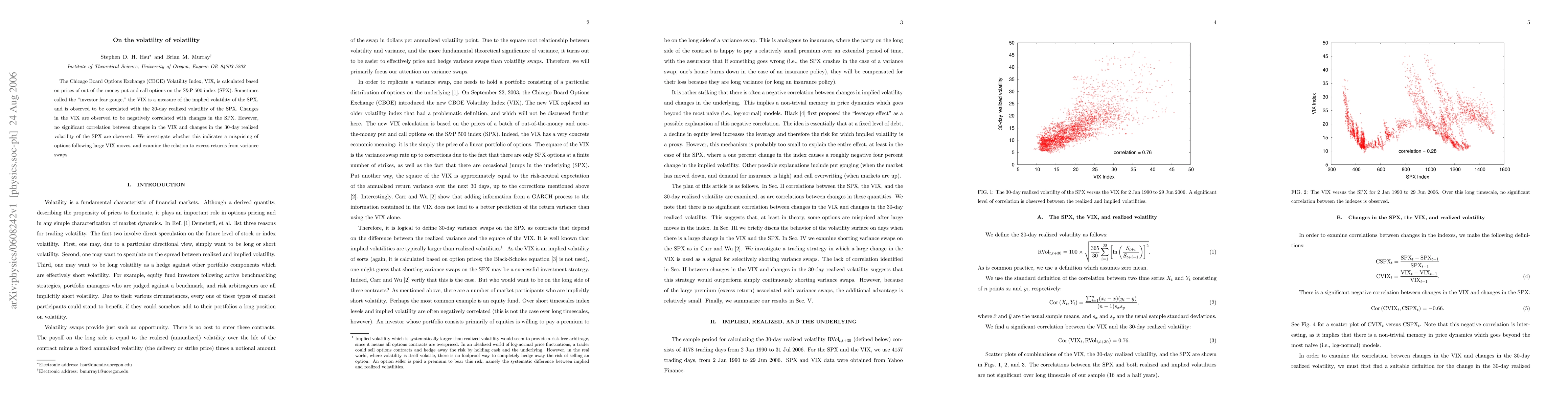

The Chicago Board Options Exchange (CBOE) Volatility Index, VIX, is

calculated based on prices of out-of-the-money put and call options on the S&P

500 index (SPX). Sometimes called the "investor fear gauge," the VIX is a

measure of the implied volatility of the SPX, and is observed to be correlated

with the 30-day realized volatility of the SPX. Changes in the VIX are observed

to be negatively correlated with changes in the SPX. However, no significant

correlation between changes in the VIX and changes in the 30-day realized

volatility of the SPX are observed. We investigate whether this indicates a

mispricing of options following large VIX moves, and examine the relation to

excess returns from variance swaps.

Discussion 0