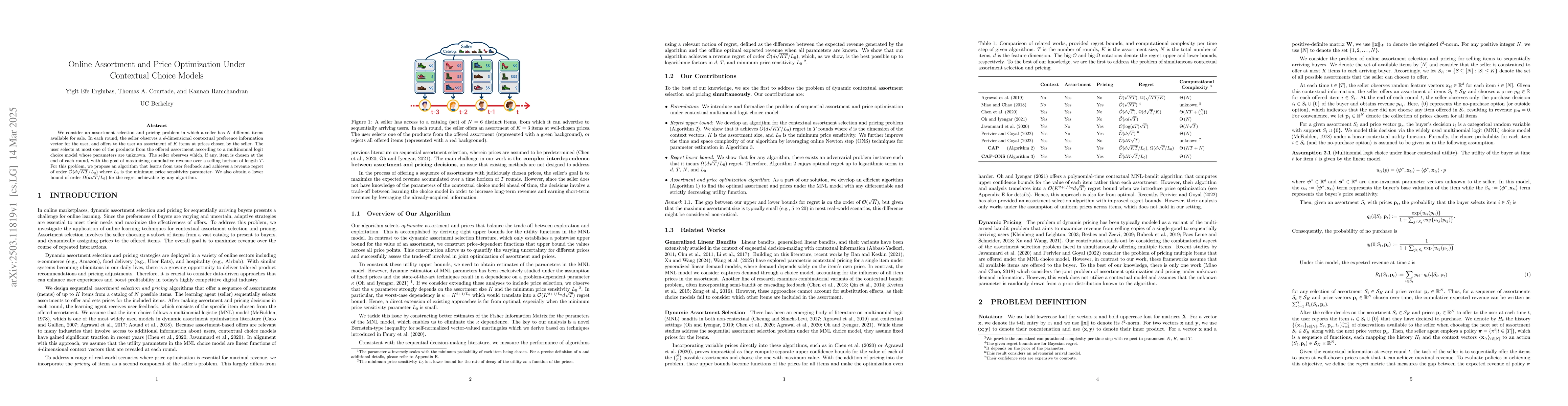

We consider an assortment selection and pricing problem in which a seller has

$N$ different items available for sale. In each round, the seller observes a

$d$-dimensional contextual preference information vector for the user, and

offers to the user an assortment of $K$ items at prices chosen by the seller.

The user selects at most one of the products from the offered assortment

according to a multinomial logit choice model whose parameters are unknown. The

seller observes which, if any, item is chosen at the end of each round, with

the goal of maximizing cumulative revenue over a selling horizon of length $T$.

For this problem, we propose an algorithm that learns from user feedback and

achieves a revenue regret of order $\widetilde{O}(d \sqrt{K T} / L_0 )$ where

$L_0$ is the minimum price sensitivity parameter. We also obtain a lower bound

of order $\Omega(d \sqrt{T}/ L_0)$ for the regret achievable by any algorithm.

Discussion 0