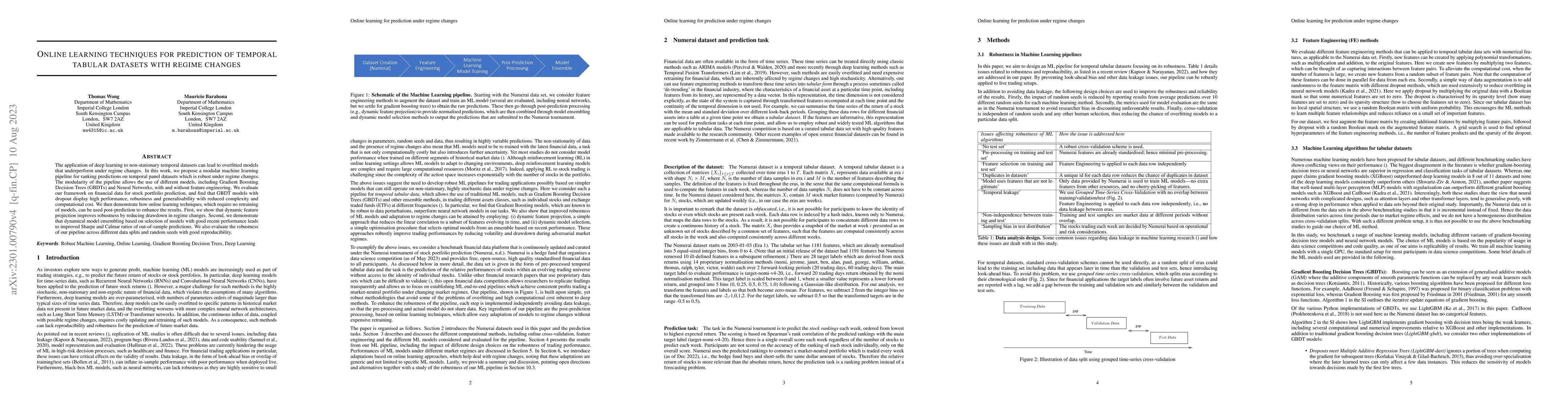

The application of deep learning to non-stationary temporal datasets can lead

to overfitted models that underperform under regime changes. In this work, we

propose a modular machine learning pipeline for ranking predictions on temporal

panel datasets which is robust under regime changes. The modularity of the

pipeline allows the use of different models, including Gradient Boosting

Decision Trees (GBDTs) and Neural Networks, with and without feature

engineering. We evaluate our framework on financial data for stock portfolio

prediction, and find that GBDT models with dropout display high performance,

robustness and generalisability with reduced complexity and computational cost.

We then demonstrate how online learning techniques, which require no retraining

of models, can be used post-prediction to enhance the results. First, we show

that dynamic feature projection improves robustness by reducing drawdown in

regime changes. Second, we demonstrate that dynamical model ensembling based on

selection of models with good recent performance leads to improved Sharpe and

Calmar ratios of out-of-sample predictions. We also evaluate the robustness of

our pipeline across different data splits and random seeds with good

reproducibility.

Discussion 0