Online Resource Allocation with Convex-set Machine-Learned Advice

Publication

Metrics

AI Quick Summary

This paper proposes a framework for online resource allocation that leverages machine-learned advice represented by a convex uncertainty set. It introduces C-Pareto optimal algorithms balancing consistent and robust performance ratios, extending classical fixed protection level algorithms, and demonstrates superior performance over benchmarks through numerical studies.

Paper Preview

Abstract

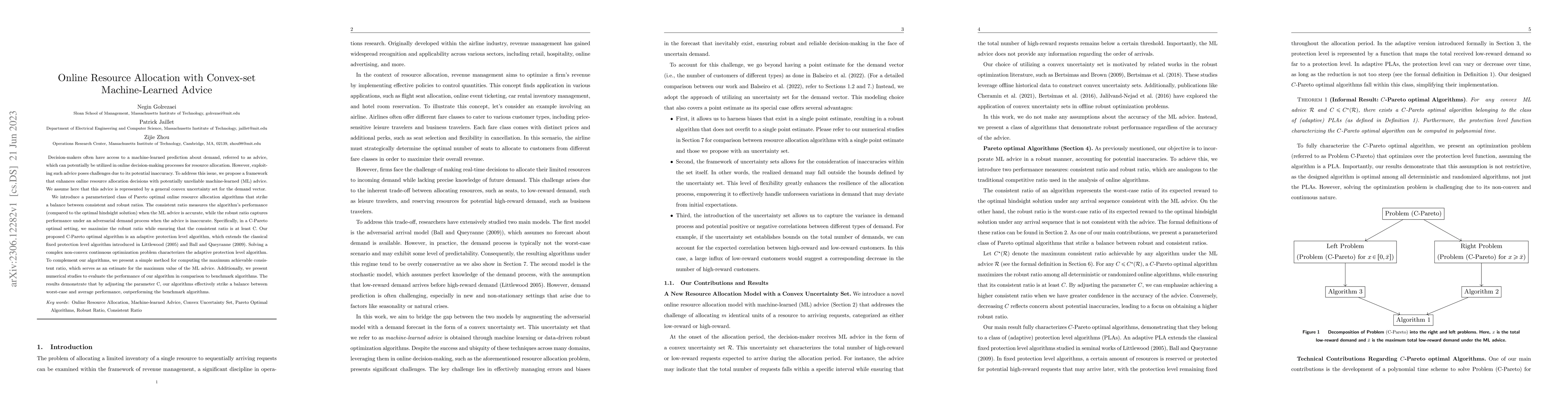

Decision-makers often have access to a machine-learned prediction about demand, referred to as advice, which can potentially be utilized in online decision-making processes for resource allocation. However, exploiting such advice poses challenges due to its potential inaccuracy. To address this issue, we propose a framework that enhances online resource allocation decisions with potentially unreliable machine-learned (ML) advice. We assume here that this advice is represented by a general convex uncertainty set for the demand vector. We introduce a parameterized class of Pareto optimal online resource allocation algorithms that strike a balance between consistent and robust ratios. The consistent ratio measures the algorithm's performance (compared to the optimal hindsight solution) when the ML advice is accurate, while the robust ratio captures performance under an adversarial demand process when the advice is inaccurate. Specifically, in a C-Pareto optimal setting, we maximize the robust ratio while ensuring that the consistent ratio is at least C. Our proposed C-Pareto optimal algorithm is an adaptive protection level algorithm, which extends the classical fixed protection level algorithm introduced in Littlewood (2005) and Ball and Queyranne (2009). Solving a complex non-convex continuous optimization problem characterizes the adaptive protection level algorithm. To complement our algorithms, we present a simple method for computing the maximum achievable consistent ratio, which serves as an estimate for the maximum value of the ML advice. Additionally, we present numerical studies to evaluate the performance of our algorithm in comparison to benchmark algorithms. The results demonstrate that by adjusting the parameter C, our algorithms effectively strike a balance between worst-case and average performance, outperforming the benchmark algorithms.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0