Optimal Attack against Autoregressive Models by Manipulating the Environment

Publication

Metrics

AI Quick Summary

This paper proposes optimal adversarial attacks against autoregressive time series models using Linear Quadratic Regulator (LQR) and Model Predictive Control (MPC). The attacks manipulate the environment to steer forecasts along a target trajectory, with effectiveness demonstrated in both white-box and black-box settings.

Paper Preview

Abstract

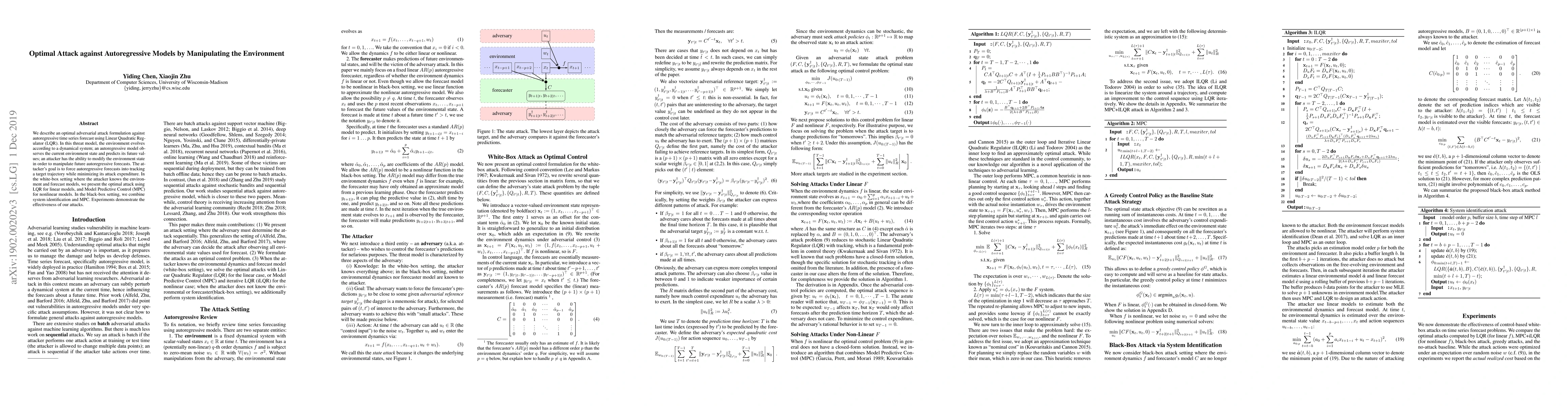

We describe an optimal adversarial attack formulation against autoregressive time series forecast using Linear Quadratic Regulator (LQR). In this threat model, the environment evolves according to a dynamical system; an autoregressive model observes the current environment state and predicts its future values; an attacker has the ability to modify the environment state in order to manipulate future autoregressive forecasts. The attacker's goal is to force autoregressive forecasts into tracking a target trajectory while minimizing its attack expenditure. In the white-box setting where the attacker knows the environment and forecast models, we present the optimal attack using LQR for linear models, and Model Predictive Control (MPC) for nonlinear models. In the black-box setting, we combine system identification and MPC. Experiments demonstrate the effectiveness of our attacks.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0