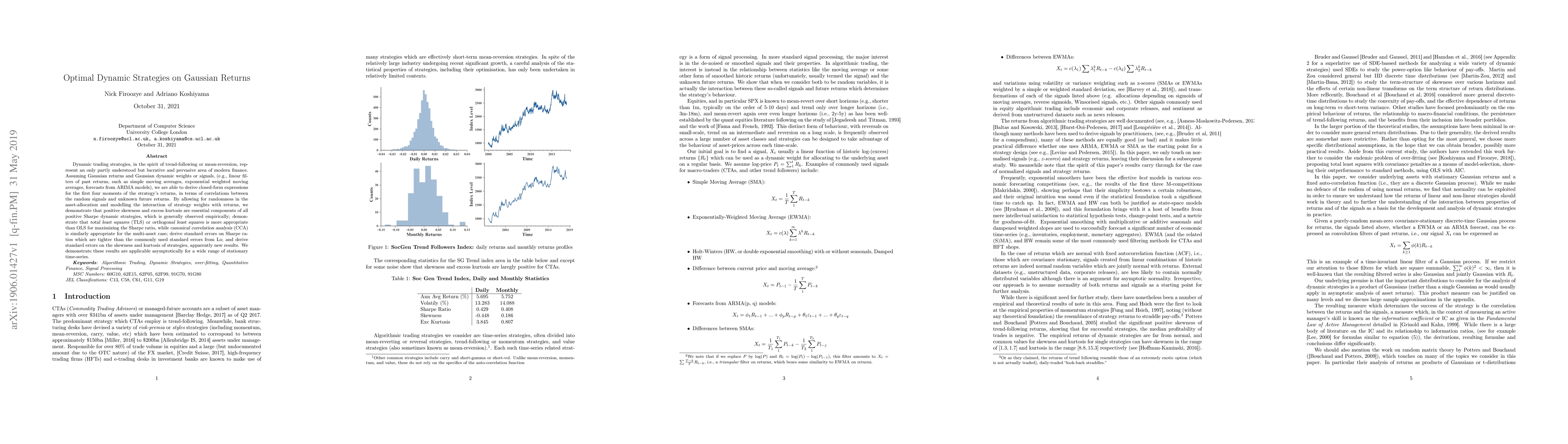

Dynamic trading strategies, in the spirit of trend-following or

mean-reversion, represent an only partly understood but lucrative and pervasive

area of modern finance. Assuming Gaussian returns and Gaussian dynamic weights

or signals, (e.g., linear filters of past returns, such as simple moving

averages, exponential weighted moving averages, forecasts from ARIMA models),

we are able to derive closed-form expressions for the first four moments of the

strategy's returns, in terms of correlations between the random signals and

unknown future returns. By allowing for randomness in the asset-allocation and

modelling the interaction of strategy weights with returns, we demonstrate that

positive skewness and excess kurtosis are essential components of all positive

Sharpe dynamic strategies, which is generally observed empirically; demonstrate

that total least squares (TLS) or orthogonal least squares is more appropriate

than OLS for maximizing the Sharpe ratio, while canonical correlation analysis

(CCA) is similarly appropriate for the multi-asset case; derive standard errors

on Sharpe ratios which are tighter than the commonly used standard errors from

Lo; and derive standard errors on the skewness and kurtosis of strategies,

apparently new results. We demonstrate these results are applicable

asymptotically for a wide range of stationary time-series.

Discussion 0