Publication

Metrics

AI Quick Summary

This paper explores optimal portfolio selection under transaction costs from a signal processing viewpoint, constructing portfolios that maximize expected growth in discrete-time markets. It introduces threshold portfolios and demonstrates their efficiency in forming an irreducible Markov chain for cumulative expected wealth calculation, ultimately optimizing parameters to yield the growth-optimal portfolio.

Paper Preview

Abstract

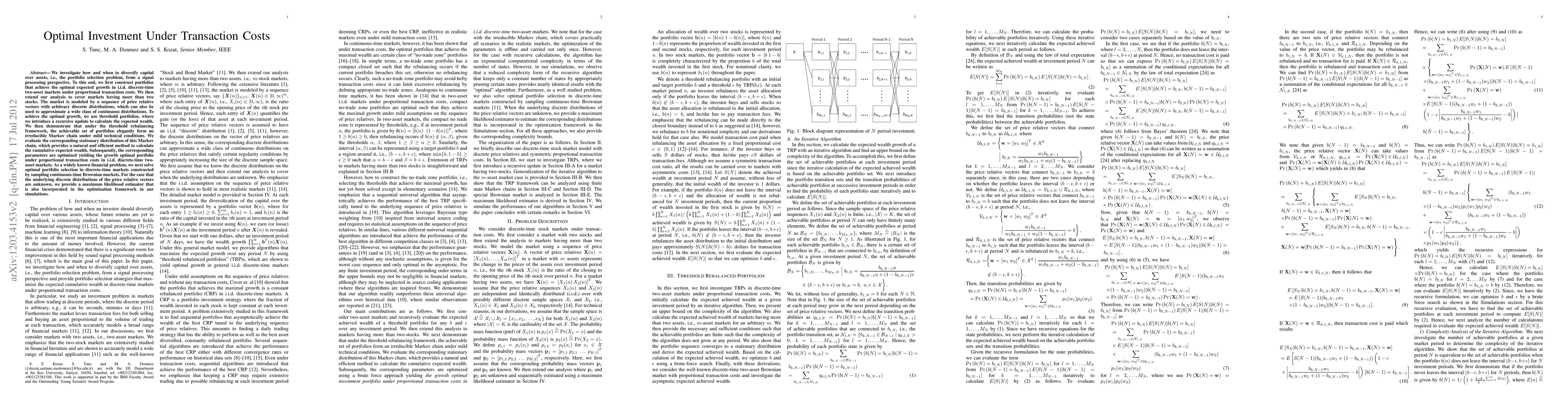

We investigate how and when to diversify capital over assets, i.e., the portfolio selection problem, from a signal processing perspective. To this end, we first construct portfolios that achieve the optimal expected growth in i.i.d. discrete-time two-asset markets under proportional transaction costs. We then extend our analysis to cover markets having more than two stocks. The market is modeled by a sequence of price relative vectors with arbitrary discrete distributions, which can also be used to approximate a wide class of continuous distributions. To achieve the optimal growth, we use threshold portfolios, where we introduce a recursive update to calculate the expected wealth. We then demonstrate that under the threshold rebalancing framework, the achievable set of portfolios elegantly form an irreducible Markov chain under mild technical conditions. We evaluate the corresponding stationary distribution of this Markov chain, which provides a natural and efficient method to calculate the cumulative expected wealth. Subsequently, the corresponding parameters are optimized yielding the growth optimal portfolio under proportional transaction costs in i.i.d. discrete-time two-asset markets. As a widely known financial problem, we next solve optimal portfolio selection in discrete-time markets constructed by sampling continuous-time Brownian markets. For the case that the underlying discrete distributions of the price relative vectors are unknown, we provide a maximum likelihood estimator that is also incorporated in the optimization framework in our simulations.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0