Online Conformal Prediction (CP) struggles to balance temporal adaptability and structural stability. Feedback-driven methods (e.g., Adaptive Conformal Inference (ACI)) suffer from systemic marginal under-coverage and high interval variance during abrupt shifts, while temporally discounted Bayesian CP suffers from severe structural lag and uncalibrated interval bloat. We propose State-Adaptive Bayesian Conformal Prediction (SA-BCP) to achieve optimal spatio-temporal decoupling. By gating long-term temporal inertia with spatial kernel-density evidence, SA-BCP proactively expands intervals for recognized historical regimes while maintaining tight efficiency during stable states. We rigorously prove this mechanism's optimality, identifying a minimax bias-variance tradeoff governed by an evidence threshold $K$. Extensive benchmarks on volatile financial datasets (2016--2026), including AMD, Gold, and GBP/USD, demonstrate that SA-BCP consistently minimizes the strictly proper Winkler score across diverse confidence levels. Specifically, SA-BCP resolves the systematic under-coverage inherent to ACI variants while simultaneously reducing the uncalibrated interval bloat of Bayesian CP by 10\% to 37\% under high-confidence requests. By elegantly navigating this tradeoff, SA-BCP achieves an optimal balance between conditional reliability and predictive efficiency.

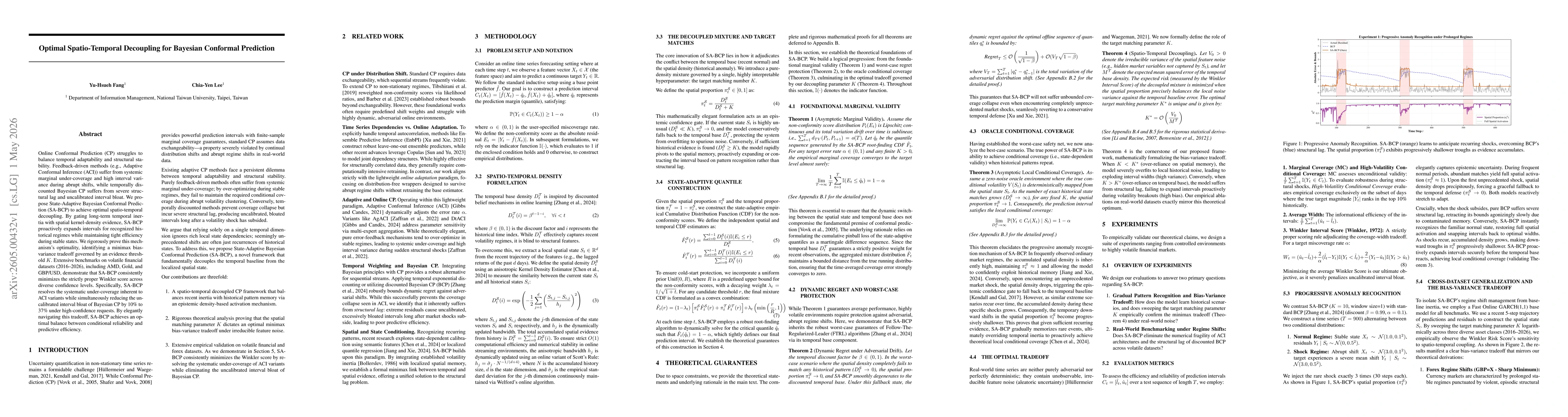

Discussion 0