Publication

Metrics

AI Quick Summary

This paper optimizes a single-asset portfolio under transaction costs using a simplified model with signal autocorrelation and cross-correlation. It explores two controls: a linear filtering parameter and a threshold determining a "no-trade" zone, aiming to minimize trade frequency for a fixed return level, finding that eliminating signal autocorrelation while maintaining a "no-trade" zone yields a locally optimal solution.

Paper Preview

Abstract

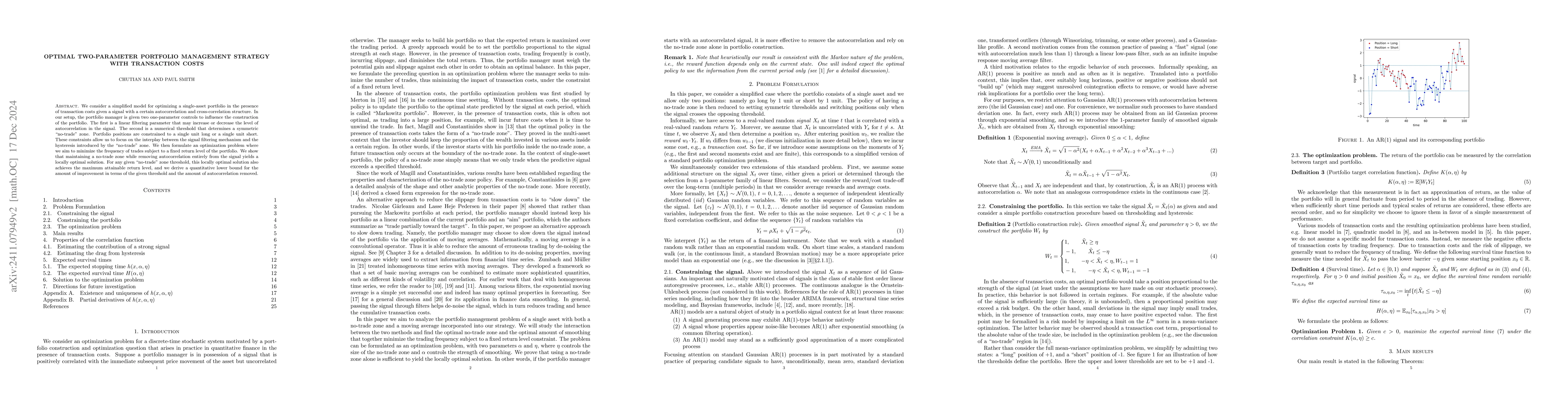

We consider a simplified model for optimizing a single-asset portfolio in the presence of transaction costs given a signal with a certain autocorrelation and cross-correlation structure. In our setup, the portfolio manager is given two one-parameter controls to influence the construction of the portfolio. The first is a linear filtering parameter that may increase or decrease the level of autocorrelation in the signal. The second is a numerical threshold that determines a symmetric ``no-trade" zone. Portfolio positions are constrained to a single unit long or a single unit short. These constraints allow us to focus on the interplay between the signal filtering mechanism and the hysteresis introduced by the ``no-trade" zone. We then formulate an optimization problem where we aim to minimize the frequency of trades subject to a fixed return level of the portfolio. We show that maintaining a no-trade zone while removing autocorrelation entirely from the signal yields a locally optimal solution. For any given ``no-trade" zone threshold, this locally optimal solution also achieves the maximum attainable return level, and we derive a quantitative lower bound for the amount of improvement in terms of the given threshold and the amount of autocorrelation removed.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0