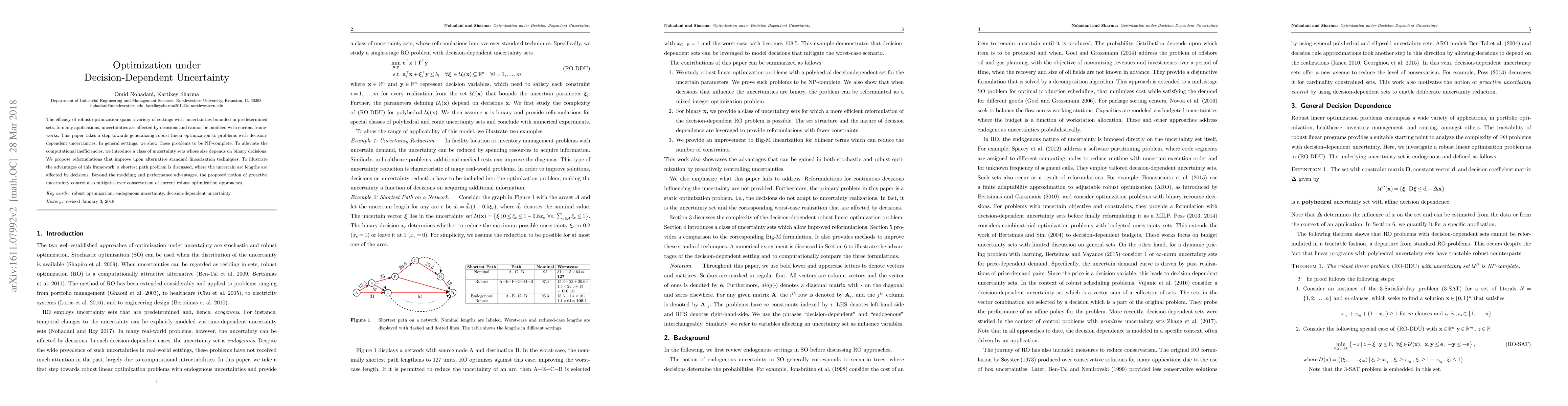

Optimization under Decision-Dependent Uncertainty

Publication

Metrics

AI Quick Summary

This paper generalizes robust linear optimization to handle decision-dependent uncertainties, demonstrating NP-completeness in general settings. It introduces reformulations to improve computational efficiency and proposes a proactive uncertainty control method that mitigates over-conservatism in robust optimization.

Paper Preview

Abstract

The efficacy of robust optimization spans a variety of settings with uncertainties bounded in predetermined sets. In many applications, uncertainties are affected by decisions and cannot be modeled with current frameworks. This paper takes a step towards generalizing robust linear optimization to problems with decision-dependent uncertainties. In general settings, we show these problems to be NP-complete. To alleviate the computational inefficiencies, we introduce a class of uncertainty sets whose size depends on binary decisions. We propose reformulations that improve upon alternative standard linearization techniques. To illustrate the advantages of this framework, a shortest path problem is discussed, where the uncertain arc lengths are affected by decisions. Beyond the modeling and performance advantages, the proposed notion of proactive uncertainty control also mitigates over conservatism of current robust optimization approaches.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0