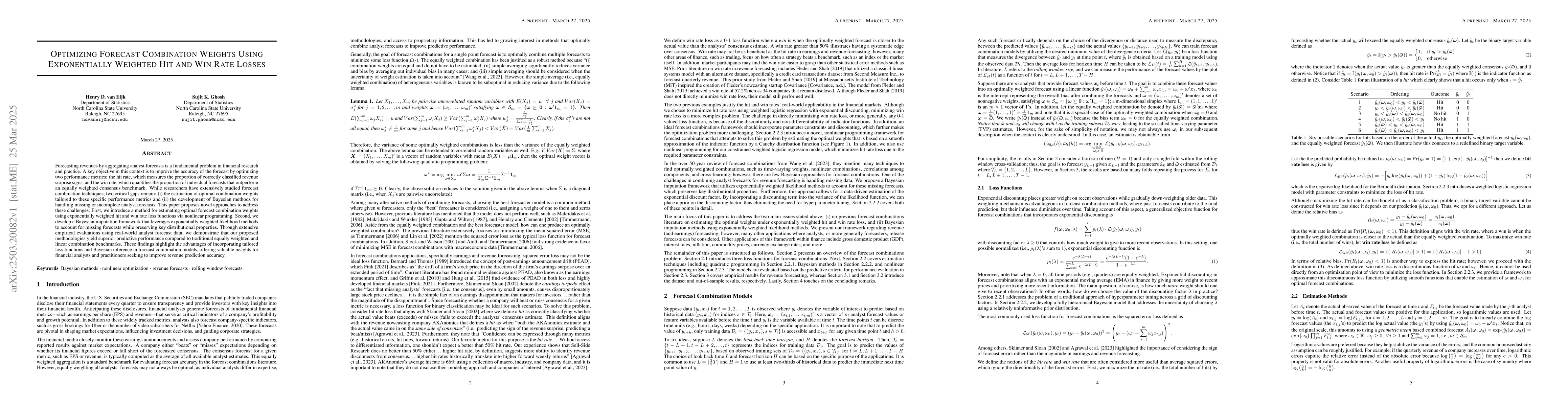

Forecasting revenues by aggregating analyst forecasts is a fundamental

problem in financial research and practice. A key objective in this context is

to improve the accuracy of the forecast by optimizing two performance metrics:

the hit rate, which measures the proportion of correctly classified revenue

surprise signs, and the win rate, which quantifies the proportion of individual

forecasts that outperform an equally weighted consensus benchmark. While

researchers have extensively studied forecast combination techniques, two

critical gaps remain: (i) the estimation of optimal combination weights

tailored to these specific performance metrics and (ii) the development of

Bayesian methods for handling missing or incomplete analyst forecasts. This

paper proposes novel approaches to address these challenges. First, we

introduce a method for estimating optimal forecast combination weights using

exponentially weighted hit and win rate loss functions via nonlinear

programming. Second, we develop a Bayesian imputation framework that leverages

exponentially weighted likelihood methods to account for missing forecasts

while preserving key distributional properties. Through extensive empirical

evaluations using real-world analyst forecast data, we demonstrate that our

proposed methodologies yield superior predictive performance compared to

traditional equally weighted and linear combination benchmarks. These findings

highlight the advantages of incorporating tailored loss functions and Bayesian

inference in forecast combination models, offering valuable insights for

financial analysts and practitioners seeking to improve revenue prediction

accuracy.

Discussion 0