Publication

Metrics

Paper Preview

Abstract

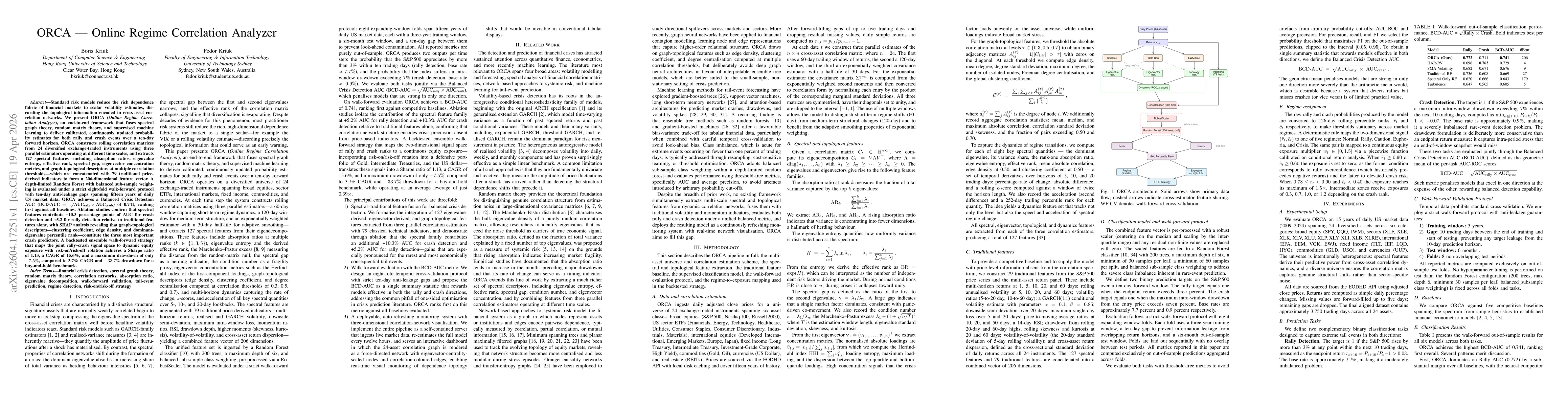

Standard risk models reduce the rich dependence structure of financial markets to scalar volatility estimates, discarding the topological information encoded in cross-asset correlation networks. We present ORCA (Online Regime Correlation Analyzer), an end-to-end framework that fuses spectral graph theory, random matrix theory, and supervised machine learning to deliver calibrated probability estimates for both rally and crash events over a ten-day forward horizon. ORCA constructs rolling correlation matrices from 24 diversified exchange-traded instruments using three parallel estimators at different time scales, and extracts 127 spectral features (absorption ratios, eigenvalue entropy, effective rank, spectral gap, eigenvector concentration, and graph-topological descriptors at multiple correlation thresholds), concatenated with 79 traditional price-derived indicators to form a 206-dimensional feature vector. A depth-limited Random Forest with balanced sub-sample weighting is evaluated under a strict eight-fold walk-forward protocol with ten-day anti-leakage gaps spanning fifteen years of daily US market data. ORCA achieves a Balanced Crisis Detection AUC (BCD-AUC, the geometric mean of rally and crash AUC) of 0.741, ranking first against all baselines. Ablation studies show that spectral features contribute +10.3 percentage points of AUC for crash detection and +5.2 for rally detection over traditional features alone, with SHAP analysis revealing that graph-topological descriptors (clustering coefficient, edge density, and dominant-eigenvalue percentile rank) are the three most important crash predictors. A backtested walk-forward strategy mapping the joint rally-crash signal to dynamic equity exposure with risk-on/risk-off rotation achieves a Sharpe ratio of 1.13, a CAGR of 15.6%, and a maximum drawdown of only -7.5%, versus 3.7% CAGR and -33.7% drawdown for buy-and-hold.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0