Overcoming Brittleness in Pareto-Optimal Learning-Augmented Algorithms

Publication

Metrics

AI Quick Summary

This paper addresses the brittleness of Pareto-optimal learning-augmented algorithms, showing their performance can degrade significantly with minor prediction errors. To mitigate this, the authors propose a framework enforcing performance smoothness through a user-specified profile, maintaining consistency/robustness tradeoffs. They apply this approach to the one-way trading problem, introducing a new Pareto-optimal algorithm that benefits from non-worst-case inputs and a dominance metric for comparing such algorithms.

Paper Preview

Abstract

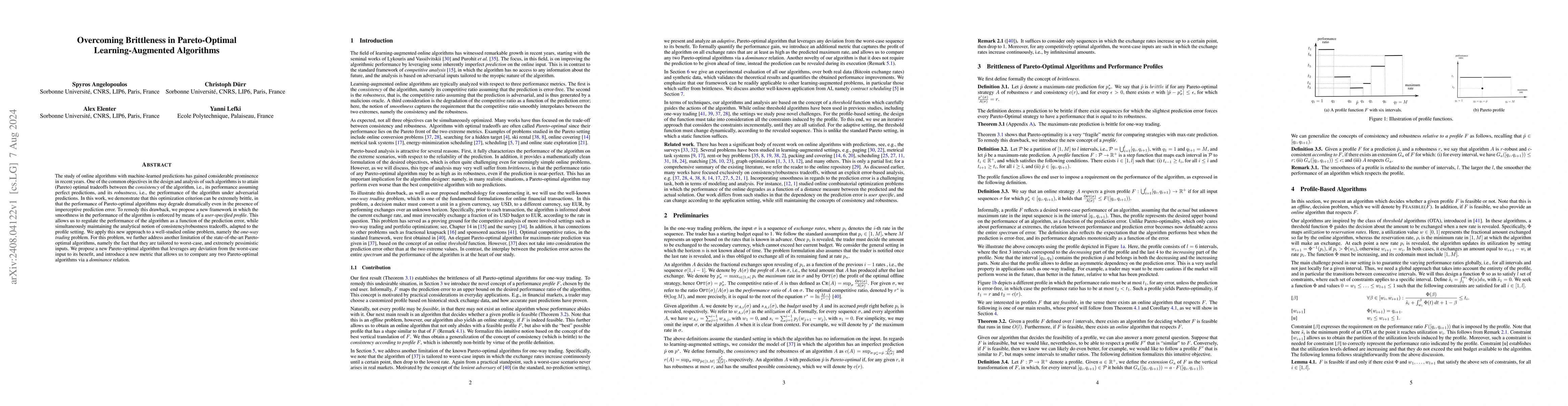

The study of online algorithms with machine-learned predictions has gained considerable prominence in recent years. One of the common objectives in the design and analysis of such algorithms is to attain (Pareto) optimal tradeoffs between the consistency of the algorithm, i.e., its performance assuming perfect predictions, and its robustness, i.e., the performance of the algorithm under adversarial predictions. In this work, we demonstrate that this optimization criterion can be extremely brittle, in that the performance of Pareto-optimal algorithms may degrade dramatically even in the presence of imperceptive prediction error. To remedy this drawback, we propose a new framework in which the smoothness in the performance of the algorithm is enforced by means of a user-specified profile. This allows us to regulate the performance of the algorithm as a function of the prediction error, while simultaneously maintaining the analytical notion of consistency/robustness tradeoffs, adapted to the profile setting. We apply this new approach to a well-studied online problem, namely the one-way trading problem. For this problem, we further address another limitation of the state-of-the-art Pareto-optimal algorithms, namely the fact that they are tailored to worst-case, and extremely pessimistic inputs. We propose a new Pareto-optimal algorithm that leverages any deviation from the worst-case input to its benefit, and introduce a new metric that allows us to compare any two Pareto-optimal algorithms via a dominance relation.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Related Papers

No references found for this paper.

Discussion 0