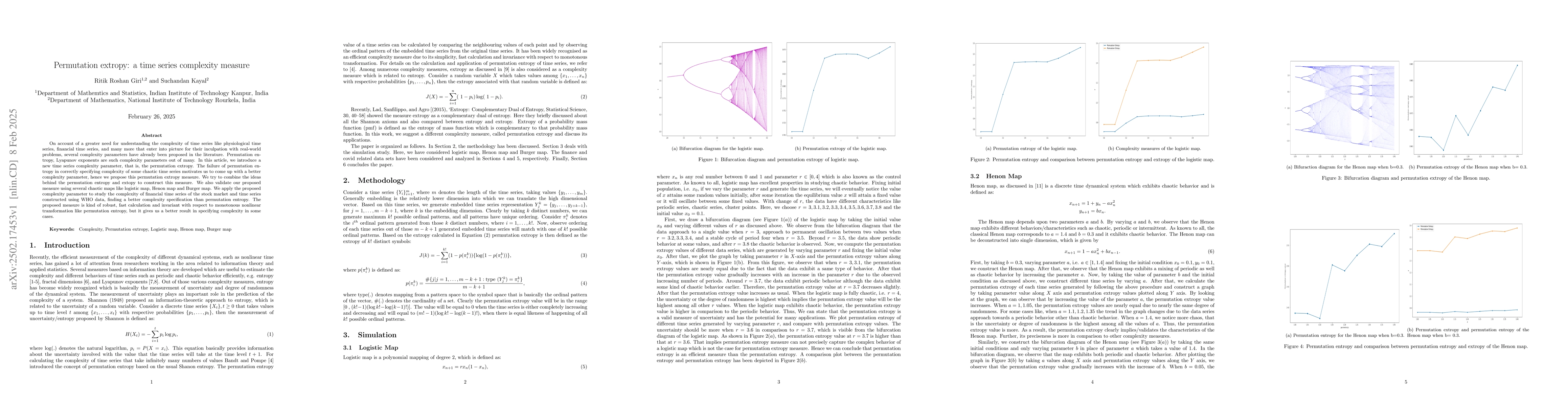

On account of a greater need for understanding the complexity of time series

like physiological time series, financial time series, and many more that enter

into picture for their inculpation with real-world problems, several complexity

parameters have already been proposed in the literature. Permutation entropy,

Lyapunov exponents are such complexity parameters out of many. In this article,

we introduce a new time series complexity parameter, that is, the permutation

extropy. The failure of permutation entropy in correctly specifying complexity

of some chaotic time series motivates us to come up with a better complexity

parameter, hence we propose this permutation extropy measure. We try to combine

the ideas behind the permutation entropy and extopy to construct this measure.

We also validate our proposed measure using several chaotic maps like logistic

map, Henon map and Burger map. We apply the proposed complexity parameter to

study the complexity of financial time series of the stock market and time

series constructed using WHO data, finding a better complexity specification

than permutation entropy. The proposed measure is kind of robust, fast

calculation and invariant with respect to monotonous nonlinear transformation

like permutation entropy, but it gives us a better result in specifying

complexity in some cases.

Discussion 0