Publication

Metrics

AI Quick Summary

This paper derives the analytical expression for the efficient frontier in portfolio optimization, including the case with a risk-free asset, and provides an R implementation with a detailed numerical example using common stocks.

Paper Preview

Abstract

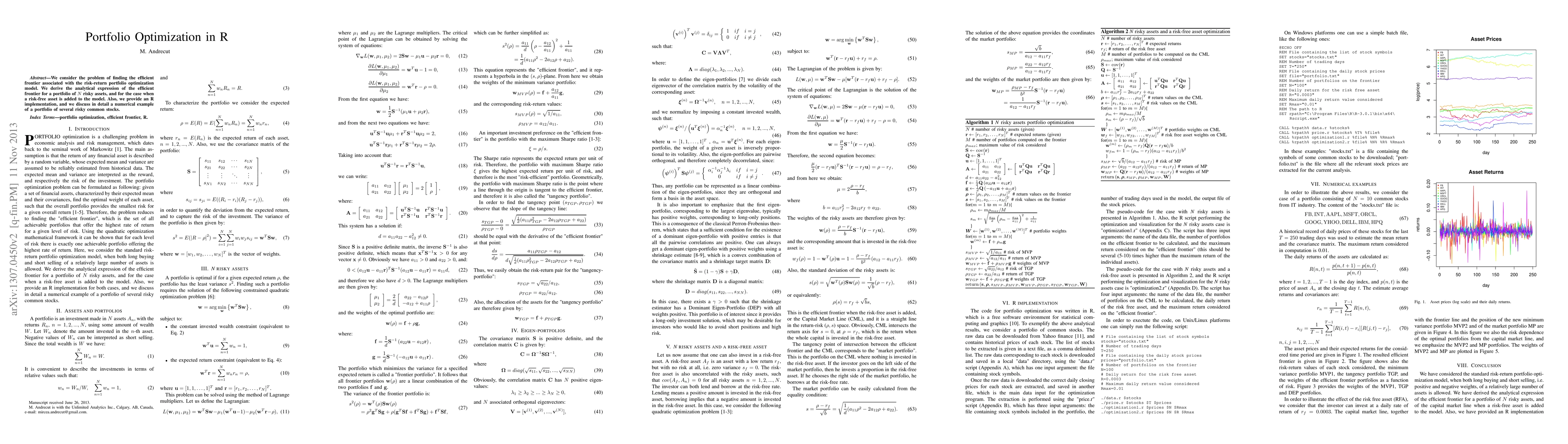

We consider the problem of finding the efficient frontier associated with the risk-return portfolio optimization model. We derive the analytical expression of the efficient frontier for a portfolio of N risky assets, and for the case when a risk-free asset is added to the model. Also, we provide an R implementation, and we discuss in detail a numerical example of a portfolio of several risky common stocks.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0