01

MethodologyHow they did it

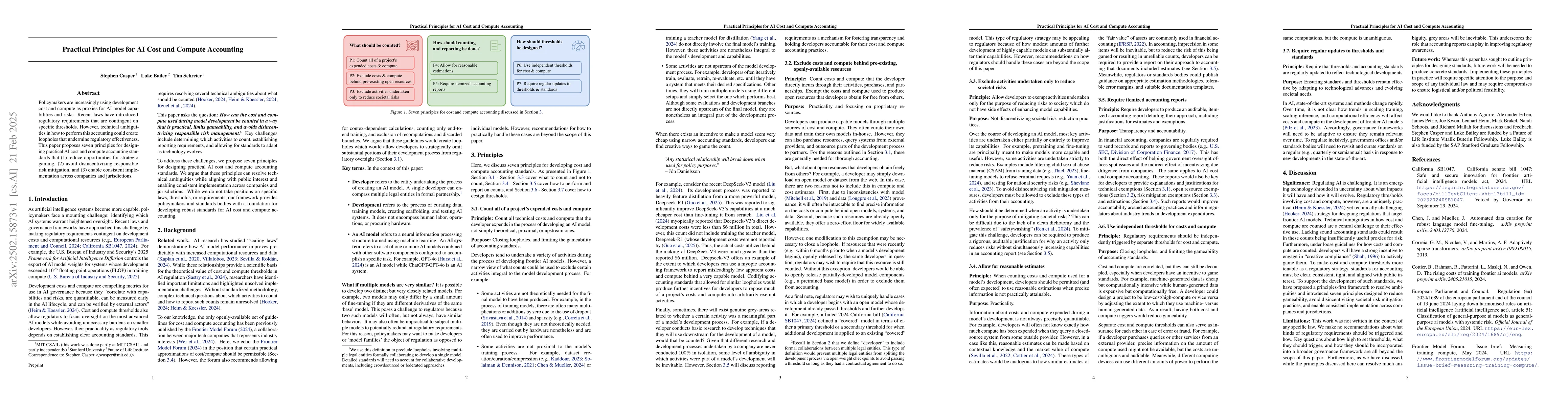

The paper proposes seven practical principles for AI cost and compute accounting standards, aiming to reduce opportunities for strategic gaming, avoid disincentivizing responsible risk mitigation, and enable consistent implementation across companies and jurisdictions.

Discussion 0