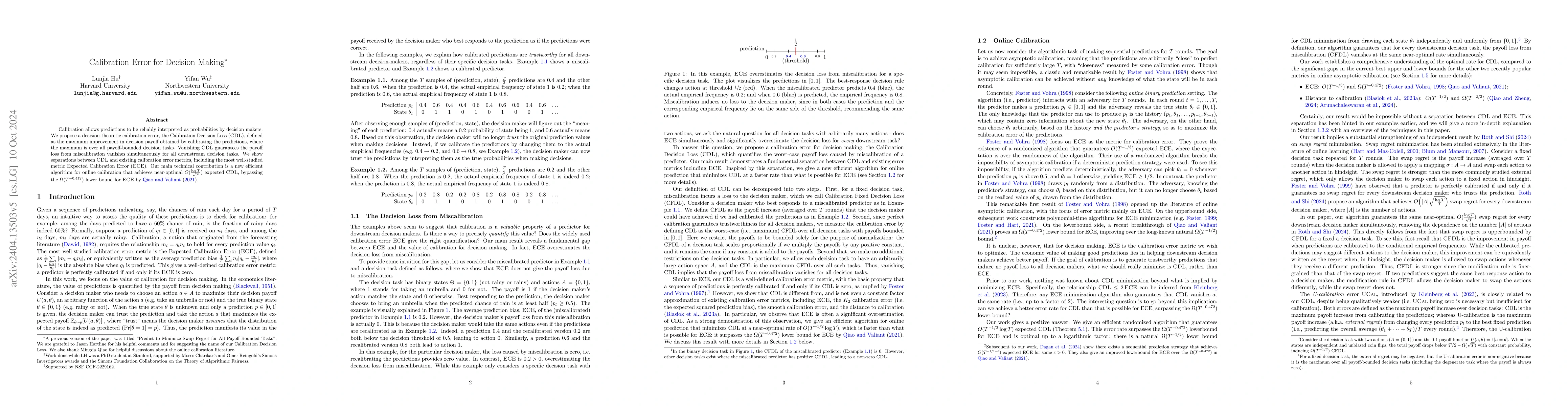

Predict to Minimize Swap Regret for All Payoff-Bounded Tasks

Publication

Metrics

AI Quick Summary

This paper presents an efficient randomized algorithm achieving $O(\sqrt{T} \log T)$ expected Maximum Swap Regret (MSR) for predicting binary events, surpassing the previous best rate and overcoming a long-standing lower bound, while discussing MSR's economic utility as a calibration error metric.

Paper Preview

Abstract

A sequence of predictions is calibrated if and only if it induces no swap regret to all down-stream decision tasks. We study the Maximum Swap Regret (MSR) of predictions for binary events: the swap regret maximized over all downstream tasks with bounded payoffs. Previously, the best online prediction algorithm for minimizing MSR is obtained by minimizing the K1 calibration error, which upper bounds MSR up to a constant factor. However, recent work (Qiao and Valiant, 2021) gives an ${\Omega}(T^{0.528})$ lower bound for the worst-case expected $K_1$ calibration error incurred by any randomized algorithm in T rounds, presenting a barrier to achieving better rates for MSR. Several relaxations of MSR have been considered to overcome this barrier, via external regret (Kleinberg et al., 2023) and regret bounds depending polynomially on the number of actions in downstream tasks (Noarov et al., 2023; Roth and Shi, 2024). We show that the barrier can be surpassed without any relaxations: we give an efficient randomized prediction algorithm that guarantees $O(\sqrt{T}logT)$ expected MSR. We also discuss the economic utility of calibration by viewing MSR as a decision-theoretic calibration error metric and study its relationship to existing metrics.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0