Predicting the Last Zero before an exponential time of a Spectrally Negative L\'evy Process

Publication

Metrics

AI Quick Summary

This paper predicts the last zero passage time of a spectrally negative Lévy process before an independent exponential time in an $L_1$ sense. It generalizes the infinite horizon problem by solving an optimal prediction problem in a finite horizon setting, characterized by a non-negative, continuous, and non-increasing curve.

Paper Preview

Abstract

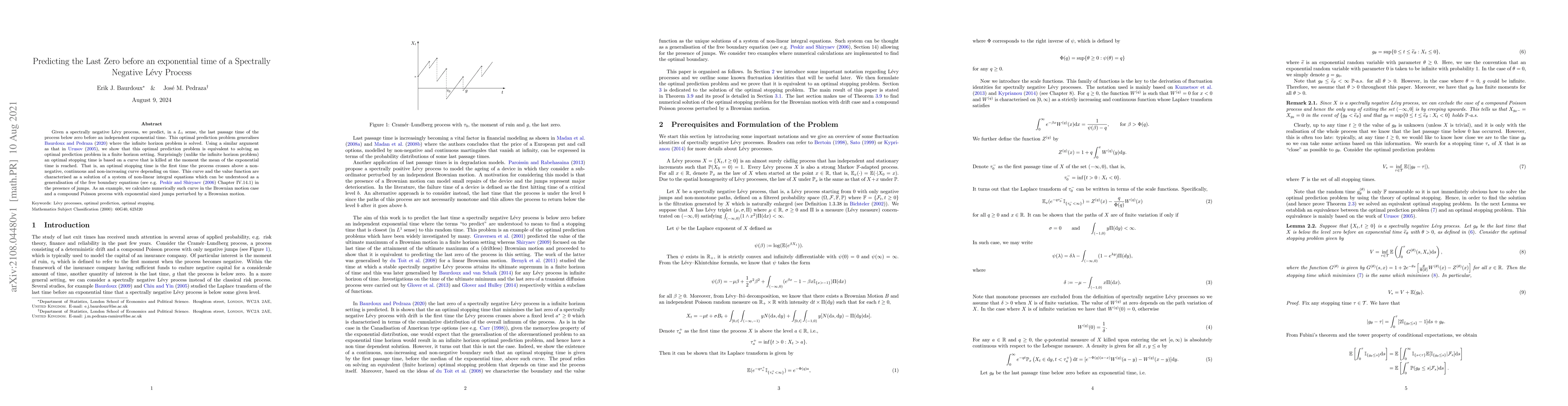

Given a spectrally negative L\'evy process, we predict, in a $L_1$ sense, the last passage time of the process below zero before an independent exponential time. This optimal prediction problem generalises Baurdoux and Pedraza (2020) where the infinite horizon problem is solved. Using a similar argument as that in Urusov (2005), we show that this optimal prediction problem is equivalent to solving an optimal prediction problem in a finite horizon setting. Surprisingly (unlike the infinite horizon problem) an optimal stopping time is based on a curve that is killed at the moment the mean of the exponential time is reached. That is, an optimal stopping time is the first time the process crosses above a non-negative, continuous and non-increasing curve depending on time. This curve and the value function are characterised as a solution of a system of non-linear integral equations which can be understood as a generalisation of the free boundary equations (see e.g. Peskir and Shiryaev (2006) Chapter IV.14.1) in the presence of jumps. As an example, we calculate numerically such curve in the Brownian motion case and a compound Poisson process with exponential sized jumps perturbed by a Brownian motion.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0