Prediction Risk and Estimation Risk of the Ridgeless Least Squares Estimator under General Assumptions on Regression Errors

Publication

Metrics

AI Quick Summary

This paper examines prediction and estimation risks of ridgeless least squares estimators under general regression error assumptions, including clustered or serial dependence. It highlights that overparameterization can provide benefits even in complex data settings like time series, panel, and grouped data, with variance-covariance matrix trace summarizing estimation difficulties.

Paper Preview

Abstract

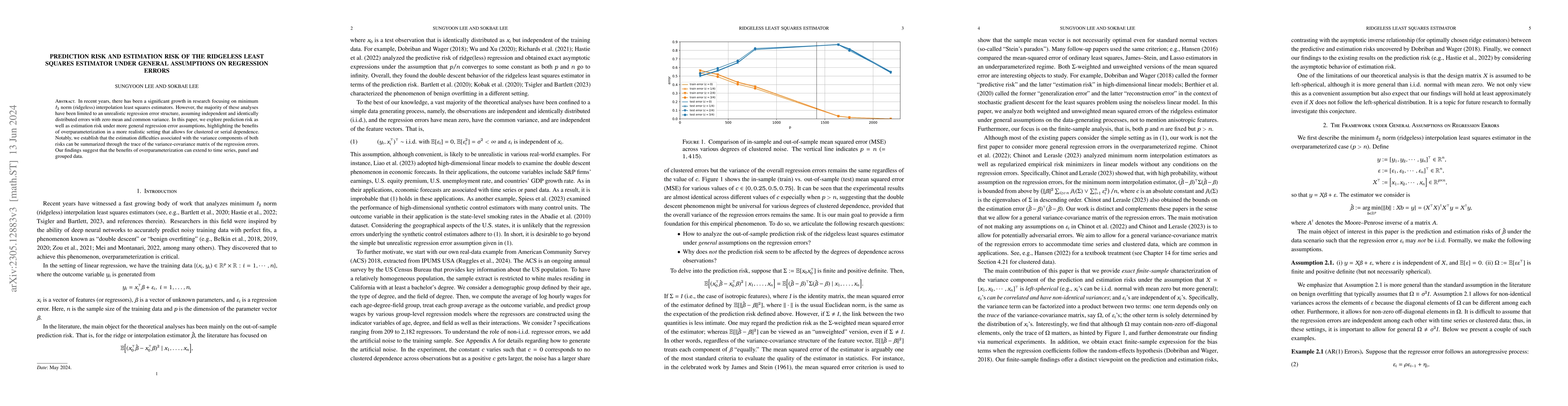

In recent years, there has been a significant growth in research focusing on minimum $\ell_2$ norm (ridgeless) interpolation least squares estimators. However, the majority of these analyses have been limited to an unrealistic regression error structure, assuming independent and identically distributed errors with zero mean and common variance. In this paper, we explore prediction risk as well as estimation risk under more general regression error assumptions, highlighting the benefits of overparameterization in a more realistic setting that allows for clustered or serial dependence. Notably, we establish that the estimation difficulties associated with the variance components of both risks can be summarized through the trace of the variance-covariance matrix of the regression errors. Our findings suggest that the benefits of overparameterization can extend to time series, panel and grouped data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0