Predictive Modeling: An Optimized and Dynamic Solution Framework for Systematic Value Investing

Publication

Metrics

AI Quick Summary

This paper proposes predictive modeling as an optimized framework for systematic value investing, employing dynamic features and financial metrics. A 31-year backtest demonstrates its performance compared to a traditional quantitative value strategy, with further enhancements shown using an expanded set of predictor variables.

Paper Preview

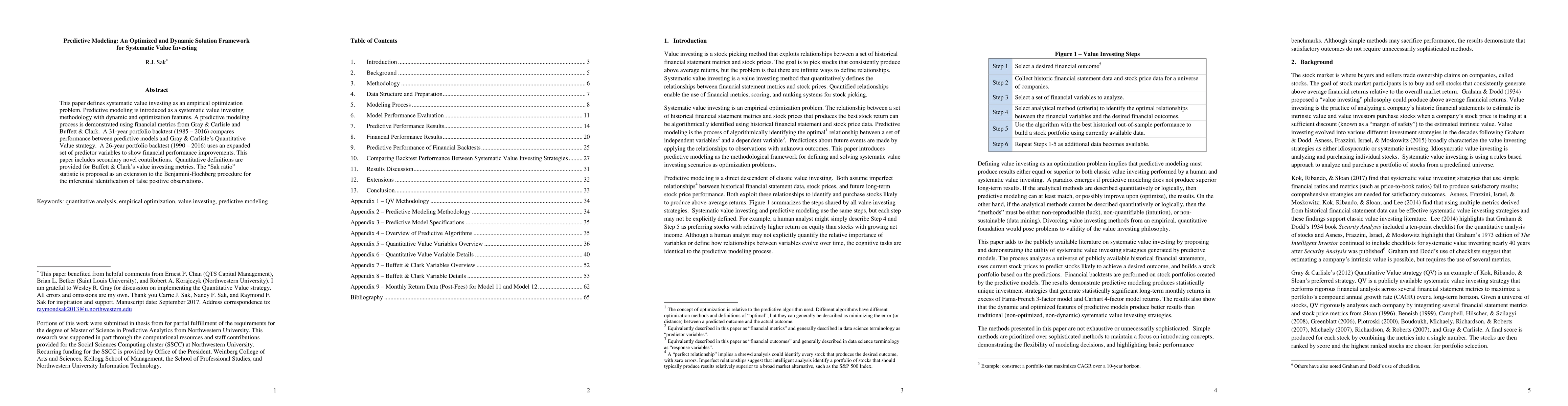

Abstract

This paper defines systematic value investing as an empirical optimization problem. Predictive modeling is introduced as a systematic value investing methodology with dynamic and optimization features. A predictive modeling process is demonstrated using financial metrics from Gray & Carlisle and Buffett & Clark. A 31-year portfolio backtest (1985 - 2016) compares performance between predictive models and Gray & Carlisle's Quantitative Value strategy. A 26-year portfolio backtest (1990 - 2016) uses an expanded set of predictor variables to show financial performance improvements. This paper includes secondary novel contributions. Quantitative definitions are provided for Buffett & Clark's value investing metrics. The "Sak ratio" is proposed as an extension to the Benjamini-Hochberg procedure for the inferential identification of false positive observations.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0