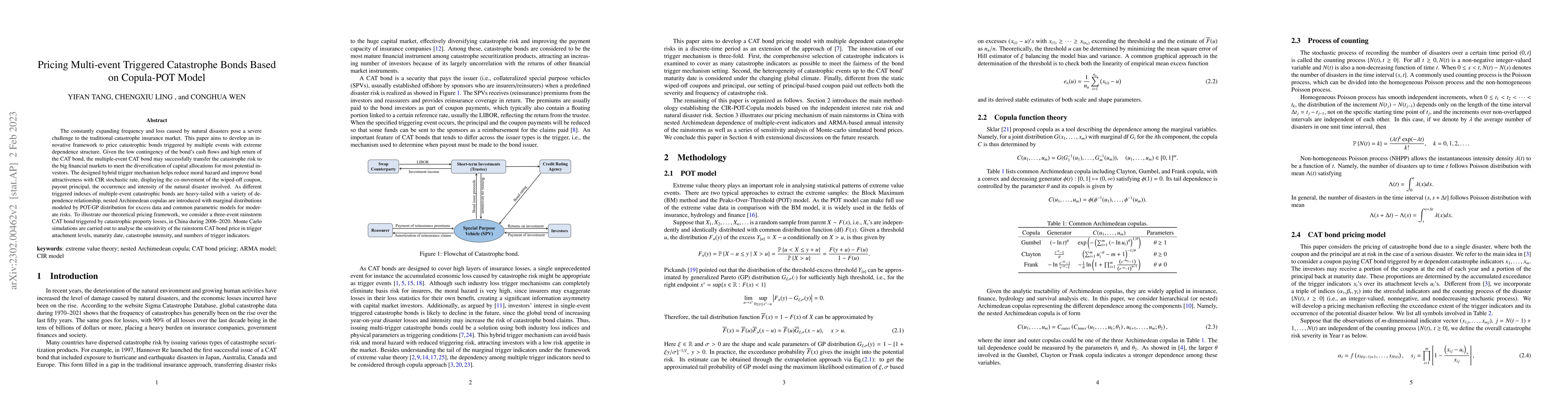

The constantly expanding frequency and loss affected by natural disasters

pose a severe challenge to the traditional catastrophe insurance market. This

paper aims to develop an innovative framework of pricing catastrophic bonds

triggered by multiple events with extreme dependence structure. Given the low

contingency of the bond's cash flows and high return, the multiple-event CAT

bond may successfully transfer the catastrophe risk to the big financial

markets meeting the diversification of capital allocations for most potential

investors. The designed hybrid trigger mechanism helps reduce moral hazard and

improve bond attractiveness with CIR stochastic rate, displaying the

co-movement of the wiped-off coupon, payout principal, the occurrence and

intensity of the natural disaster involved. As different triggered indexes of

multiple-event catastrophic bonds are heavy-tailed with a variety of dependence

relationship, nested Archimedean copulas are introduced with marginal

distributions modeled by POT-GP distribution for excess data and common

parametric models for moderate risks. To illustrate our theoretical pricing

framework, we consider a three-event rainstorm CAT bond triggered by

catastrophic property losses, in China during 2006--2020. Monte Carlo

simulations are conducted for the sensitivity analysis of the rainstorm CAT

bond price is also in trigger attachment levels, maturity date, catastrophe

intensity, and numbers of trigger indicators.

Discussion 0