Authors

Summary

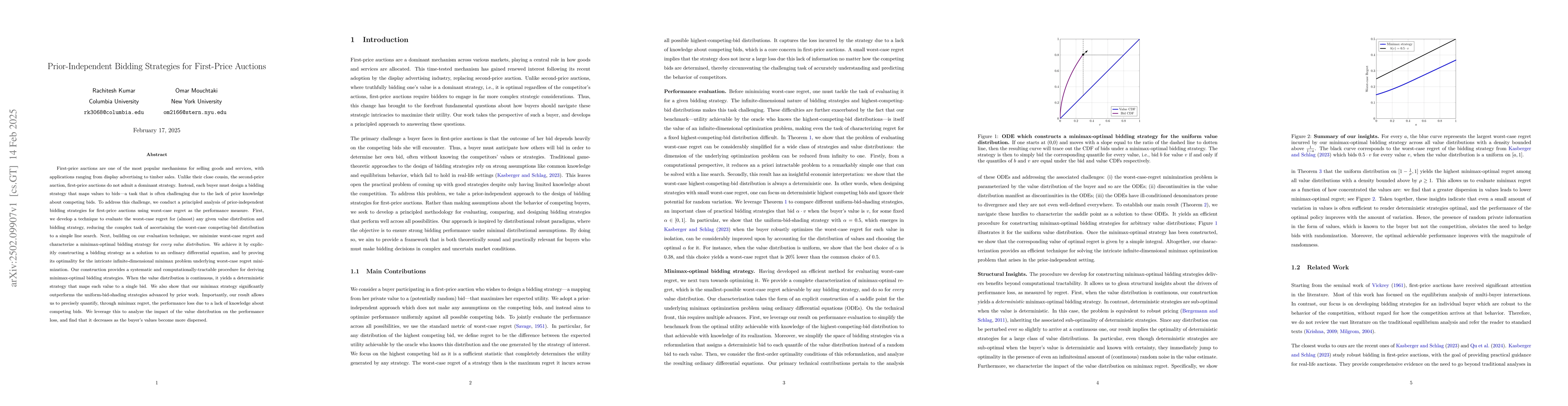

First-price auctions are one of the most popular mechanisms for selling goods and services, with applications ranging from display advertising to timber sales. Unlike their close cousin, the second-price auction, first-price auctions do not admit a dominant strategy. Instead, each buyer must design a bidding strategy that maps values to bids -- a task that is often challenging due to the lack of prior knowledge about competing bids. To address this challenge, we conduct a principled analysis of prior-independent bidding strategies for first-price auctions using worst-case regret as the performance measure. First, we develop a technique to evaluate the worst-case regret for (almost) any given value distribution and bidding strategy, reducing the complex task of ascertaining the worst-case competing-bid distribution to a simple line search. Next, building on our evaluation technique, we minimize worst-case regret and characterize a minimax-optimal bidding strategy for every value distribution. We achieve it by explicitly constructing a bidding strategy as a solution to an ordinary differential equation, and by proving its optimality for the intricate infinite-dimensional minimax problem underlying worst-case regret minimization. Our construction provides a systematic and computationally-tractable procedure for deriving minimax-optimal bidding strategies. When the value distribution is continuous, it yields a deterministic strategy that maps each value to a single bid. We also show that our minimax strategy significantly outperforms the uniform-bid-shading strategies advanced by prior work. Our result allows us to precisely quantify, through minimax regret, the performance loss due to a lack of knowledge about competing bids. We leverage this to analyze the impact of the value distribution on the performance loss, and find that it decreases as the buyer's values become more dispersed.

AI Key Findings

Generated Jun 11, 2025

Methodology

The paper employs a prior-independent framework for designing bidding strategies in first-price auctions, utilizing worst-case regret as the performance metric. It avoids strong distributional assumptions about competing bids, making it robust to uncertainty in auction environments.

Key Results

- Characterization of a minimax-optimal bidding strategy Q* for first-price auctions that significantly outperforms uniform-bid-shading strategies.

- Efficient procedure for evaluating and comparing worst-case regret for arbitrary strategies.

- Minimax-optimal bidding strategy Q* is shown to be computationally tractable as a solution to an ordinary differential equation (ODE).

- The minimax-optimal strategy Q* is deterministic for continuous value distributions.

- Quantification of the buyer's minimax regret, providing a metric for assessing the impact of informational deficiency in bidding environments.

Significance

This research is significant as it provides a robust and principled approach for buyers to contend with uncertainty about competition, whether due to lack of data or rapid market changes, thereby improving performance in first-price auctions.

Technical Contribution

The paper presents a novel approach to designing bidding strategies in first-price auctions by minimizing worst-case regret, providing a systematic and computationally tractable method to construct minimax-optimal strategies.

Novelty

The work distinguishes itself by developing a prior-independent framework that does not require strong distributional assumptions about competing bids, unlike previous approaches, and by characterizing minimax-optimal bidding strategies using worst-case regret.

Limitations

- The method relies on assumptions about the underlying value distribution and may not generalize well to highly skewed or complex distributions.

- The analysis assumes full information about the value distribution, which might not always be available in practice.

Future Work

- Investigate the performance of the proposed strategies under more complex value distributions.

- Explore extensions to multi-unit auctions or more general auction formats.

Paper Details

PDF Preview

Similar Papers

Found 4 papersStrategically-Robust Learning Algorithms for Bidding in First-Price Auctions

Jon Schneider, Balasubramanian Sivan, Rachitesh Kumar

Leveraging the Hints: Adaptive Bidding in Repeated First-Price Auctions

Wei Zhang, Tsachy Weissman, Zhengyuan Zhou et al.

Adaptive Bidding Policies for First-Price Auctions with Budget Constraints under Non-stationarity

Jiashuo Jiang, Yige Wang

No citations found for this paper.

Comments (0)