Publication

Metrics

AI Quick Summary

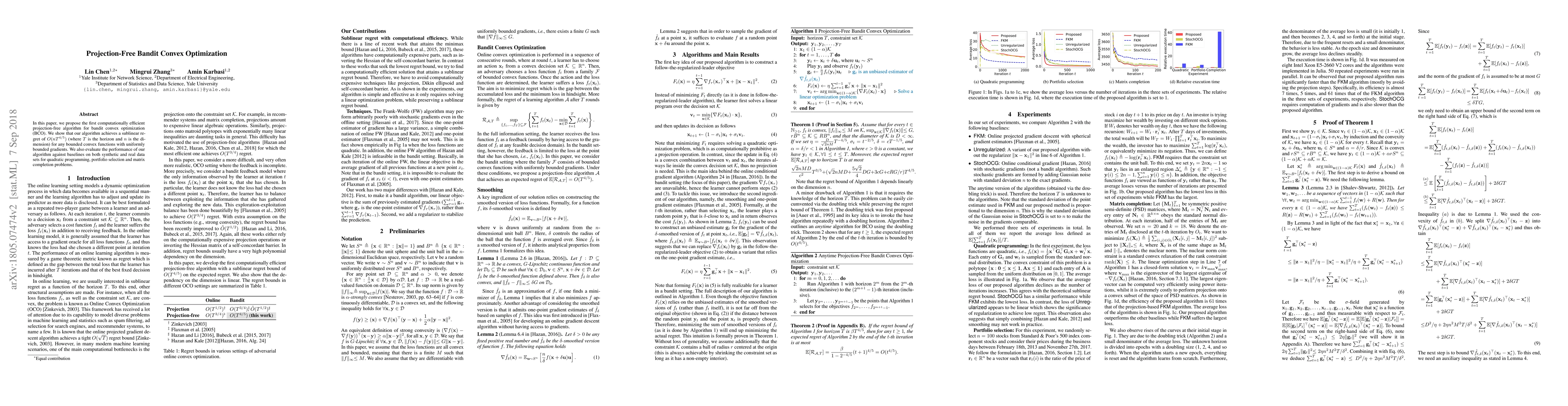

This paper introduces a projection-free algorithm for bandit convex optimization, achieving a sublinear regret of $O(nT^{4/5})$. The performance is tested against baselines on synthetic and real datasets for problems like quadratic programming, portfolio selection, and matrix completion.

Paper Preview

Abstract

In this paper, we propose the first computationally efficient projection-free algorithm for bandit convex optimization (BCO). We show that our algorithm achieves a sublinear regret of $O(nT^{4/5})$ (where $T$ is the horizon and $n$ is the dimension) for any bounded convex functions with uniformly bounded gradients. We also evaluate the performance of our algorithm against baselines on both synthetic and real data sets for quadratic programming, portfolio selection and matrix completion problems.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0