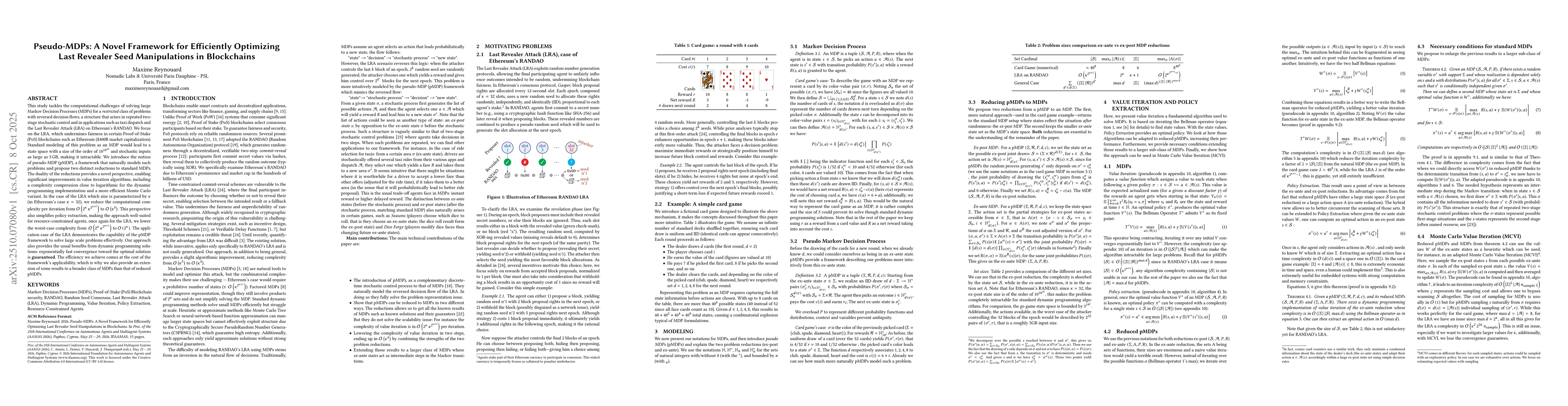

This study tackles the computational challenges of solving Markov Decision

Processes (MDPs) for a restricted class of problems. It is motivated by the

Last Revealer Attack (LRA), which undermines fairness in some Proof-of-Stake

(PoS) blockchains such as Ethereum (\$400B market capitalization). We introduce

pseudo-MDPs (pMDPs) a framework that naturally models such problems and propose

two distinct problem reductions to standard MDPs. One problem reduction

provides a novel, counter-intuitive perspective, and combining the two problem

reductions enables significant improvements in dynamic programming algorithms

such as value iteration. In the case of the LRA which size is parameterized by

$\kappa$ (in Ethereum's case $\kappa$= 325), we reduce the computational

complexity from $O(2^\kappa \kappa^{2^{\kappa+2}})$ to $O(\kappa^4)$ (per

iteration). This solution also provide the usual benefits from Dynamic

Programming solutions: exponentially fast convergence toward the optimal

solution is guaranteed. The dual perspective also simplifies policy extraction,

making the approach well-suited for resource-constrained agents who can operate

with very limited memory and computation once the problem has been solved.

Furthermore, we generalize those results to a broader class of MDPs, enhancing

their applicability. The framework is validated through two case studies: a

fictional card game and the LRA on the Ethereum random seed consensus protocol.

These applications demonstrate the framework's ability to solve large-scale

problems effectively while offering actionable insights into optimal

strategies. This work advances the study of MDPs and contributes to

understanding security vulnerabilities in blockchain systems.

Discussion 0