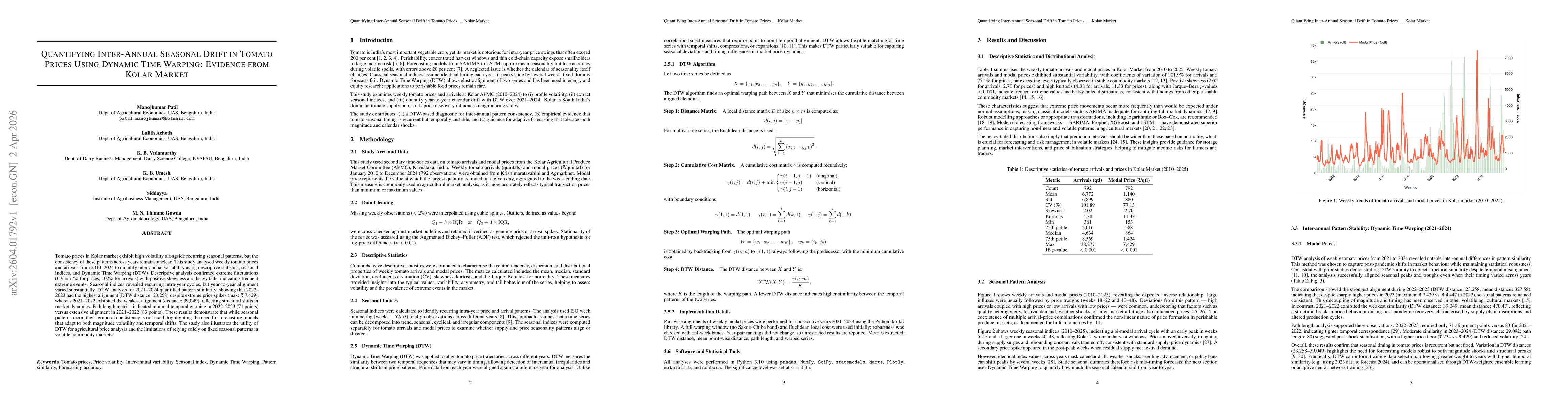

Tomato prices in Kolar market exhibit high volatility alongside recurring seasonal patterns, but the consistency of these patterns across years remains unclear. This study analysed weekly tomato prices and arrivals from 2010-2024 to quantify inter-annual variability using descriptive statistics, seasonal indices, and Dynamic Time Warping (DTW). Descriptive analysis confirmed extreme fluctuations (CV = 77% for prices, 102% for arrivals) with positive skewness and heavy tails, indicating frequent extreme events. Seasonal indices revealed recurring intra-year cycles, but year-to-year alignment varied substantially. DTW analysis for 2021-2024 quantified pattern similarity, showing that 2022-2023 had the highest alignment (DTW distance: 23,258) despite extreme price spikes, whereas 2021-2022 exhibited the weakest alignment (distance: 39,049), reflecting structural shifts in market dynamics. Path length metrics indicated minimal temporal warping in 2022-2023 (71 points) versus extensive alignment in 2021-2022 (83 points). These results demonstrate that while seasonal patterns recur, their temporal consistency is not fixed, highlighting the need for forecasting models that adapt to both magnitude volatility and temporal shifts. The study also illustrates the utility of DTW for agricultural price analysis and the limitations of relying solely on fixed seasonal patterns in volatile commodity markets.

Discussion 0