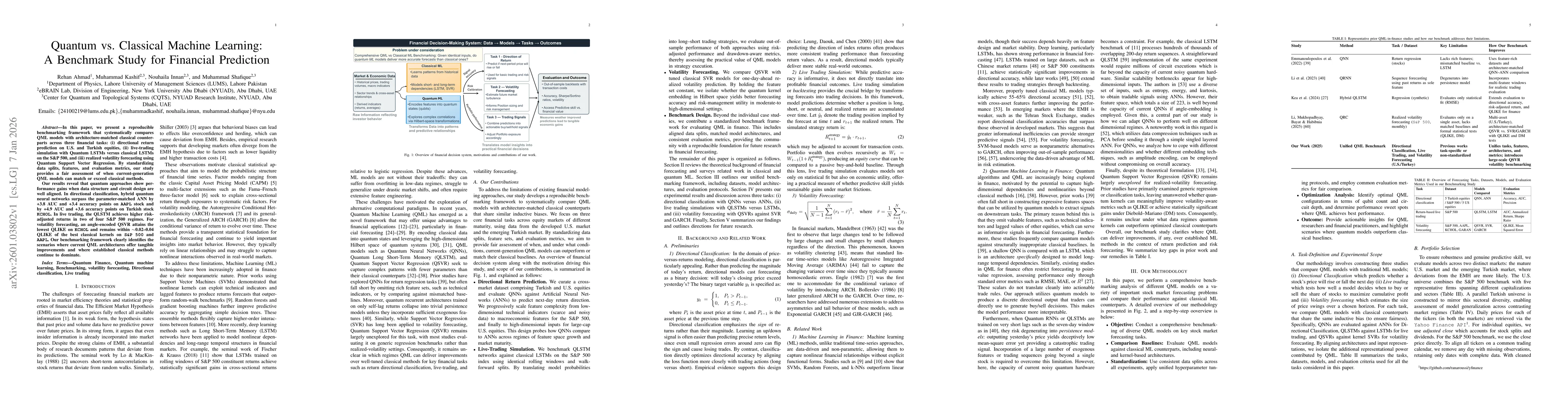

In this paper, we present a reproducible benchmarking framework that systematically compares QML models with architecture-matched classical counterparts across three financial tasks: (i) directional return prediction on U.S. and Turkish equities, (ii) live-trading simulation with Quantum LSTMs versus classical LSTMs on the S\&P 500, and (iii) realized volatility forecasting using Quantum Support Vector Regression. By standardizing data splits, features, and evaluation metrics, our study provides a fair assessment of when current-generation QML models can match or exceed classical methods. Our results reveal that quantum approaches show performance gains when data structure and circuit design are well aligned. In directional classification, hybrid quantum neural networks surpass the parameter-matched ANN by \textbf{+3.8 AUC} and \textbf{+3.4 accuracy points} on \texttt{AAPL} stock and by \textbf{+4.9 AUC} and \textbf{+3.6 accuracy points} on Turkish stock \texttt{KCHOL}. In live trading, the QLSTM achieves higher risk-adjusted returns in \textbf{two of four} S\&P~500 regimes. For volatility forecasting, an angle-encoded QSVR attains the \textbf{lowest QLIKE} on \texttt{KCHOL} and remains within $\sim$0.02-0.04 QLIKE of the best classical kernels on \texttt{S\&P~500} and \texttt{AAPL}. Our benchmarking framework clearly identifies the scenarios where current QML architectures offer tangible improvements and where established classical methods continue to dominate.

Discussion 0