This paper develops a quasi-maximum likelihood estimator for genuinely unbalanced dynamic network panel data models with individual fixed effects. We propose a model that accommodates contemporaneous and lagged network spillovers, temporal dependence, and a listing effect that activates upon a unit's first appearance in the panel. We establish the consistency of the QMLE as both $N$ and $T$ go to infinity, derive its asymptotic distribution, and identify an asymptotic bias arising from incidental parameters when $N$ is asymptotically large relative to $T$. Based on the asymptotic bias expression, we propose a bias-corrected estimator that is asymptotically unbiased and normally distributed under appropriate regularity conditions. Monte Carlo experiments examine the finite sample performance of the bias-corrected estimator across different criteria, including bias, RMSE, coverage probability, and the normality of the estimator. The empirical application to Airbnb listings from New Zealand and New York City reveals region-specific patterns in spatial and temporal price transmission, illustrating the importance of modeling genuine unbalancedness in dynamic network settings.

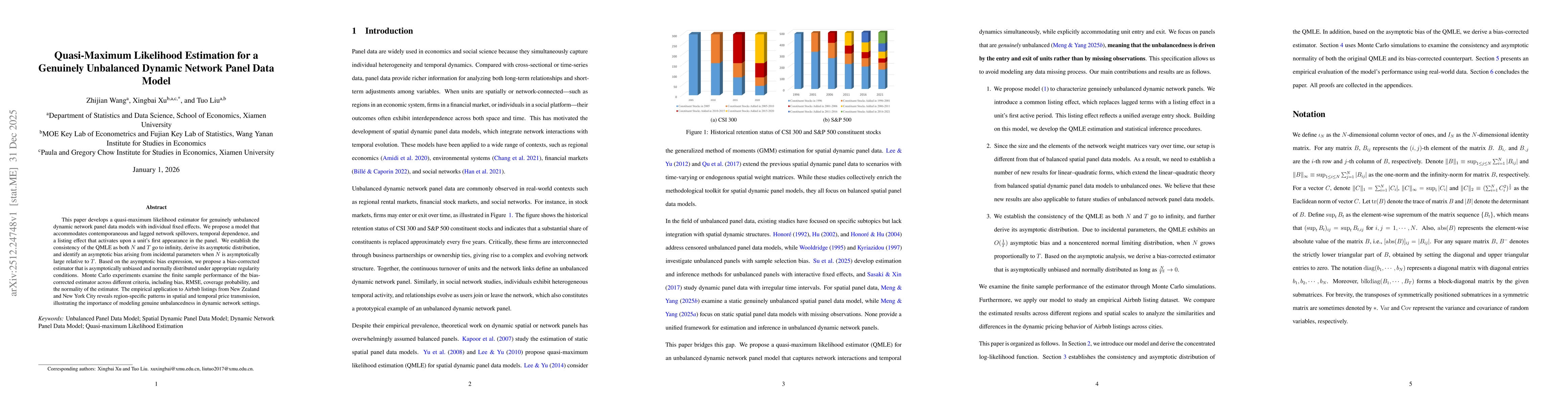

Discussion 0