RACORN-K: Risk-Aversion Pattern Matching-based Portfolio Selection

Publication

Metrics

AI Quick Summary

RACORN-K algorithm improves portfolio selection by penalizing risk, delivering notable improvements in return, Sharp ratio, and maximum drawdown on volatile markets.

Paper Preview

Abstract

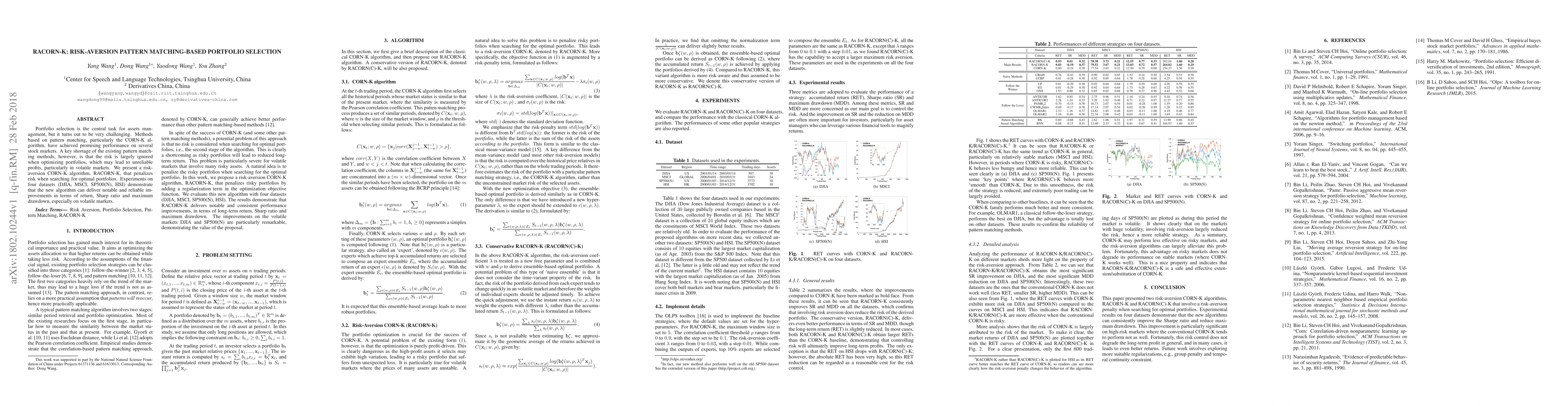

Portfolio selection is the central task for assets management, but it turns out to be very challenging. Methods based on pattern matching, particularly the CORN-K algorithm, have achieved promising performance on several stock markets. A key shortage of the existing pattern matching methods, however, is that the risk is largely ignored when optimizing portfolios, which may lead to unreliable profits, particularly in volatile markets. We present a risk-aversion CORN-K algorithm, RACORN-K, that penalizes risk when searching for optimal portfolios. Experiments on four datasets (DJIA, MSCI, SP500(N), HSI) demonstrate that the new algorithm can deliver notable and reliable improvements in terms of return, Sharp ratio and maximum drawdown, especially on volatile markets.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0