Publication

Metrics

AI Quick Summary

This paper studies how to find a random variable X that makes the time it takes for a Brownian motion to reach a certain boundary have a specific distribution, and shows that such variables exist, are unique, and can be found using certain methods.

Paper Preview

Abstract

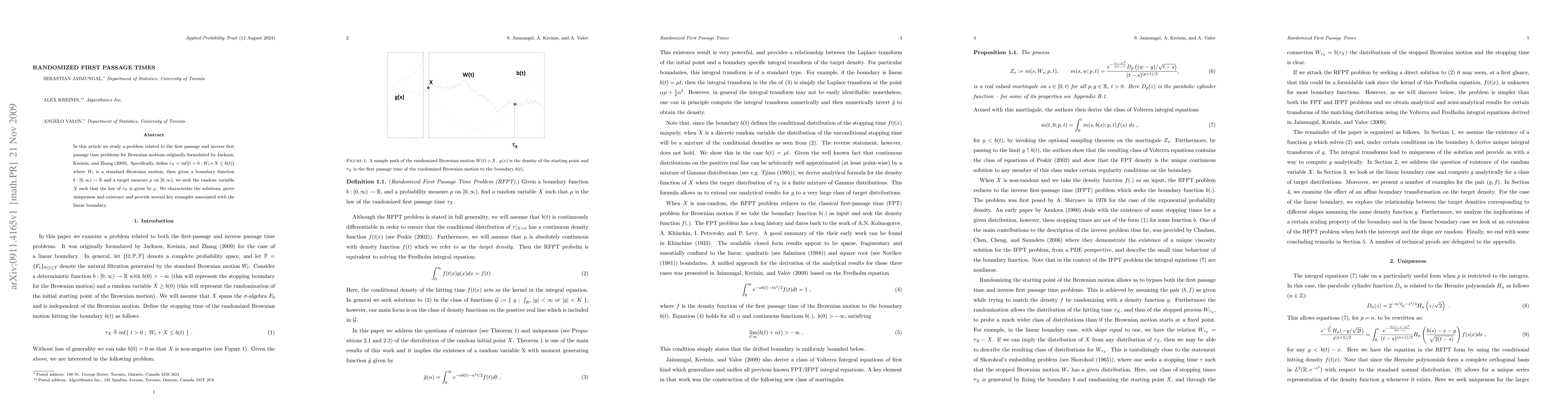

In this article we study a problem related to the first passage and inverse first passage time problems for Brownian motions originally formulated by Jackson, Kreinin and Zhang (2009). Specifically, define $\tau_X = \inf\{t>0:W_t + X \le b(t) \}$ where $W_t$ is a standard Brownian motion, then given a boundary function $b:[0,\infty) \to \RR$ and a target measure $\mu$ on $[0,\infty)$, we seek the random variable $X$ such that the law of $\tau_X$ is given by $\mu$. We characterize the solutions, prove uniqueness and existence and provide several key examples associated with the linear boundary.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0