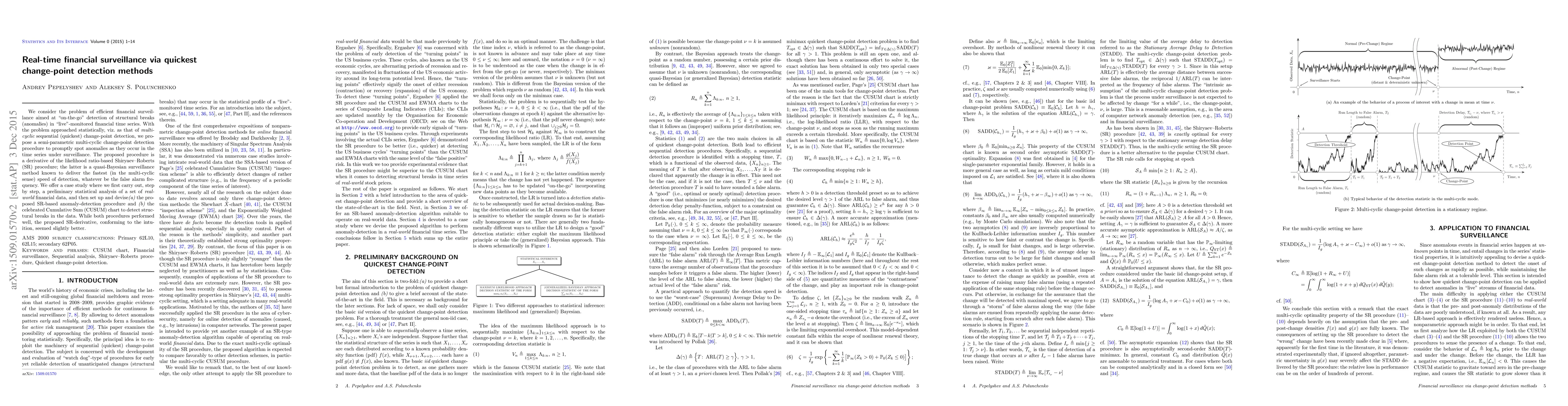

Real-time financial surveillance via quickest change-point detection methods

Publication

Metrics

AI Quick Summary

This paper proposes a semi-parametric multi-cyclic change-point detection method based on the Shiryaev-Roberts procedure for real-time financial surveillance to detect anomalies in financial time series. The proposed method is compared to the Cumulative Sum (CUSUM) chart, showing slightly better performance in detecting structural breaks in real-world financial data.

Paper Preview

Abstract

We consider the problem of efficient financial surveillance aimed at "on-the-go" detection of structural breaks (anomalies) in "live"-monitored financial time series. With the problem approached statistically, viz. as that of multi-cyclic sequential (quickest) change-point detection, we propose a semi-parametric multi-cyclic change-point detection procedure to promptly spot anomalies as they occur in the time series under surveillance. The proposed procedure is a derivative of the likelihood ratio-based Shiryaev-Roberts (SR) procedure; the latter is a quasi-Bayesian surveillance method known to deliver the fastest (in the multi-cyclic sense) speed of detection, whatever be the false alarm frequency. We offer a case study where we first carry out, step by step, statistical analysis of a set of real-world financial data, and then set up and devise (a) the proposed SR-based anomaly-detection procedure and (b) the celebrated Cumulative Sum (CUSUM) chart to detect structural breaks in the data. While both procedures performed well, the proposed SR-derivative, conforming to the intuition, seemed slightly better.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0