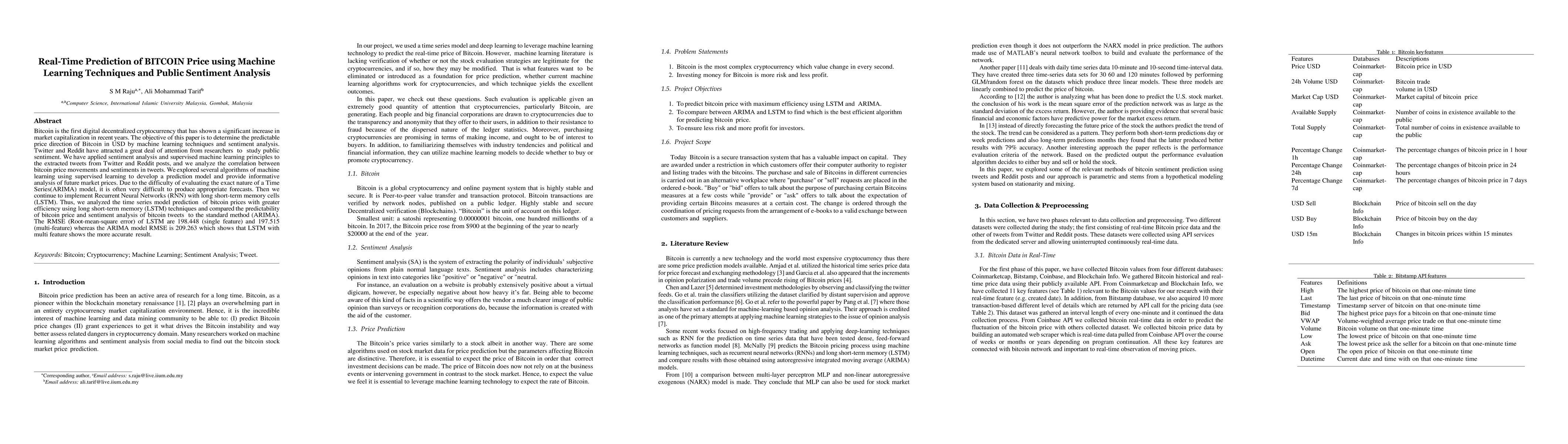

Bitcoin is the first digital decentralized cryptocurrency that has shown a

significant increase in market capitalization in recent years. The objective of

this paper is to determine the predictable price direction of Bitcoin in USD by

machine learning techniques and sentiment analysis. Twitter and Reddit have

attracted a great deal of attention from researchers to study public sentiment.

We have applied sentiment analysis and supervised machine learning principles

to the extracted tweets from Twitter and Reddit posts, and we analyze the

correlation between bitcoin price movements and sentiments in tweets. We

explored several algorithms of machine learning using supervised learning to

develop a prediction model and provide informative analysis of future market

prices. Due to the difficulty of evaluating the exact nature of a Time

Series(ARIMA) model, it is often very difficult to produce appropriate

forecasts. Then we continue to implement Recurrent Neural Networks (RNN) with

long short-term memory cells (LSTM). Thus, we analyzed the time series model

prediction of bitcoin prices with greater efficiency using long short-term

memory (LSTM) techniques and compared the predictability of bitcoin price and

sentiment analysis of bitcoin tweets to the standard method (ARIMA). The RMSE

(Root-mean-square error) of LSTM are 198.448 (single feature) and 197.515

(multi-feature) whereas the ARIMA model RMSE is 209.263 which shows that LSTM

with multi feature shows the more accurate result.

Discussion 0