Recombining binomial tree for constant elasticity of variance process

Publication

Metrics

AI Quick Summary

This paper proposes a recombining binomial tree method to price American put options under a constant elasticity of variance (CEV) process, achieving linear complexity and confirmed convergence through numerical experiments. The method emulates the CEV process using a finite difference scheme and computes the price effectively.

Paper Preview

Abstract

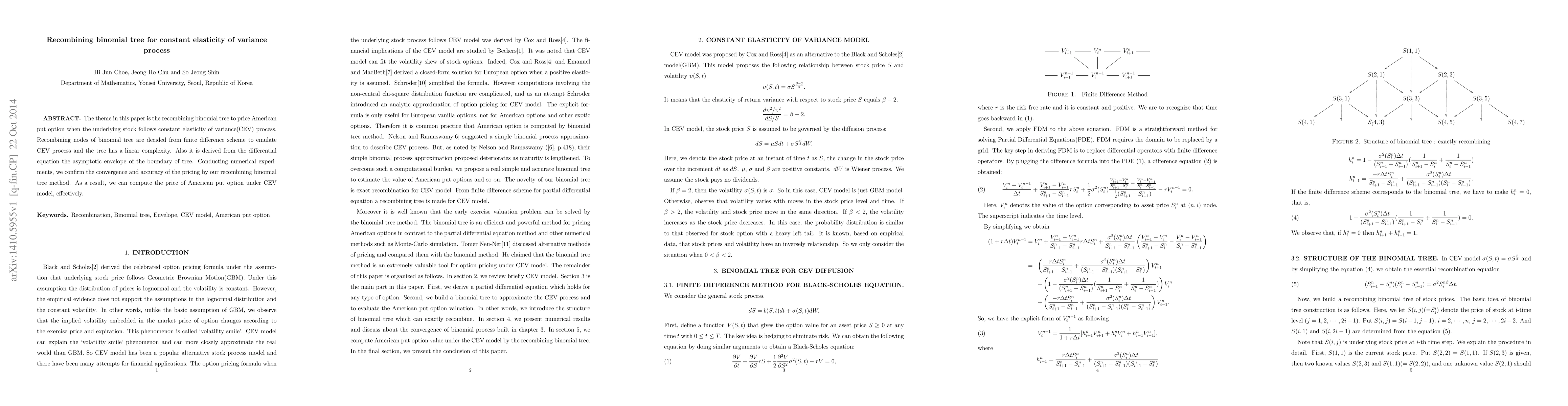

The theme in this paper is the recombining binomial tree to price American put option when the underlying stock follows constant elasticity of variance(CEV) process. Recombining nodes of binomial tree are decided from finite difference scheme to emulate CEV process and the tree has a linear complexity. Also it is derived from the differential equation the asymptotic envelope of the boundary of tree. Conducting numerical experiments, we confirm the convergence and accuracy of the pricing by our recombining binomial tree method. As a result, we can compute the price of American put option under CEV model, effectively.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0