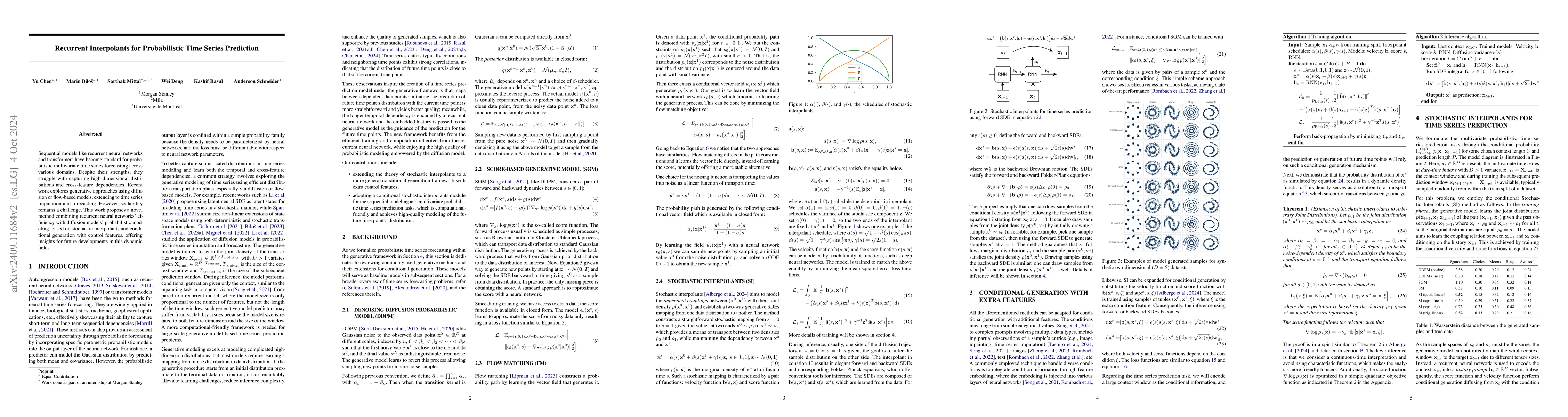

Recurrent Interpolants for Probabilistic Time Series Prediction

Publication

Metrics

AI Quick Summary

This paper proposes a novel recurrent interpolant approach that combines the computational efficiency of recurrent neural networks with the high-quality probabilistic modeling of diffusion models to tackle scalability issues in large-scale time series forecasting. The method utilizes stochastic interpolants and conditional generation frameworks to improve prediction uncertainty and efficiency.

Paper Preview

Abstract

Sequential models such as recurrent neural networks or transformer-based models became \textit{de facto} tools for multivariate time series forecasting in a probabilistic fashion, with applications to a wide range of datasets, such as finance, biology, medicine, etc. Despite their adeptness in capturing dependencies, assessing prediction uncertainty, and efficiency in training, challenges emerge in modeling high-dimensional complex distributions and cross-feature dependencies. To tackle these issues, recent works delve into generative modeling by employing diffusion or flow-based models. Notably, the integration of stochastic differential equations or probability flow successfully extends these methods to probabilistic time series imputation and forecasting. However, scalability issues necessitate a computational-friendly framework for large-scale generative model-based predictions. This work proposes a novel approach by blending the computational efficiency of recurrent neural networks with the high-quality probabilistic modeling of the diffusion model, which addresses challenges and advances generative models' application in time series forecasting. Our method relies on the foundation of stochastic interpolants and the extension to a broader conditional generation framework with additional control features, offering insights for future developments in this dynamic field.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0