01

MethodologyHow they did it

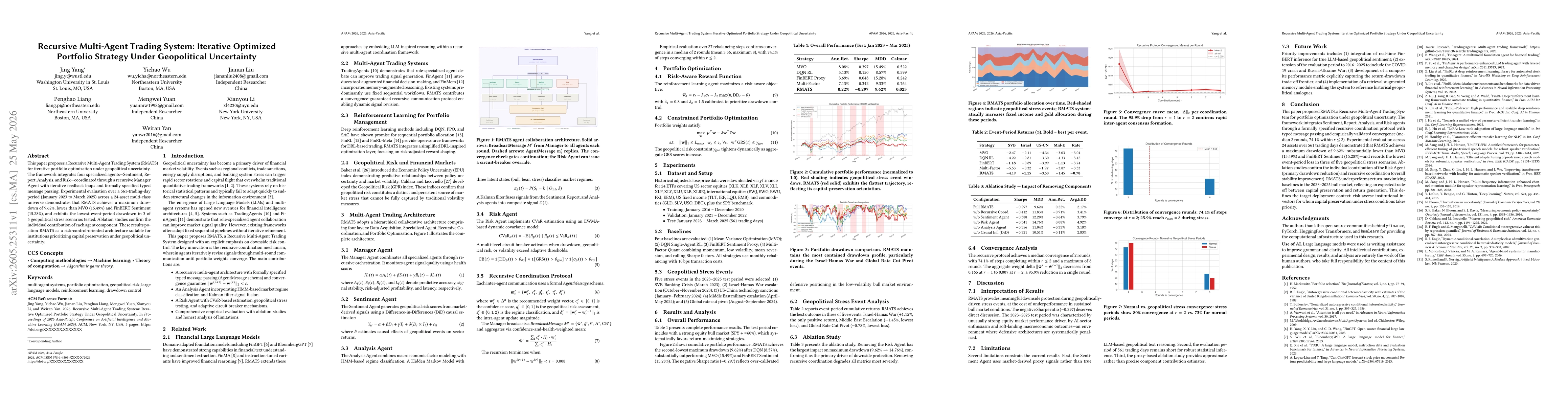

RMATS employs four specialized agents (Sentiment, Report, Analysis, Risk) coordinated by a Recursive Manager Agent via a formal AgentMessageschema. It uses a convergence-guaranteed recursive coordination protocol with typed message passing, a CVaR-based risk estimation, HMM-based regime classification, Kalman-fusion, dynamic circuit breakers, and a health score to monitor agent signal quality. Experimental evaluation over 561 trading days across 24 assets demonstrates iterative signal refinement until portfolio weights converge (||w(r+1) - w(r)||2 < epsilon).

Discussion 0